Big League Loan Sharks

How “Income-Share Agreements” Are Becoming Commonplace in Major League Sports

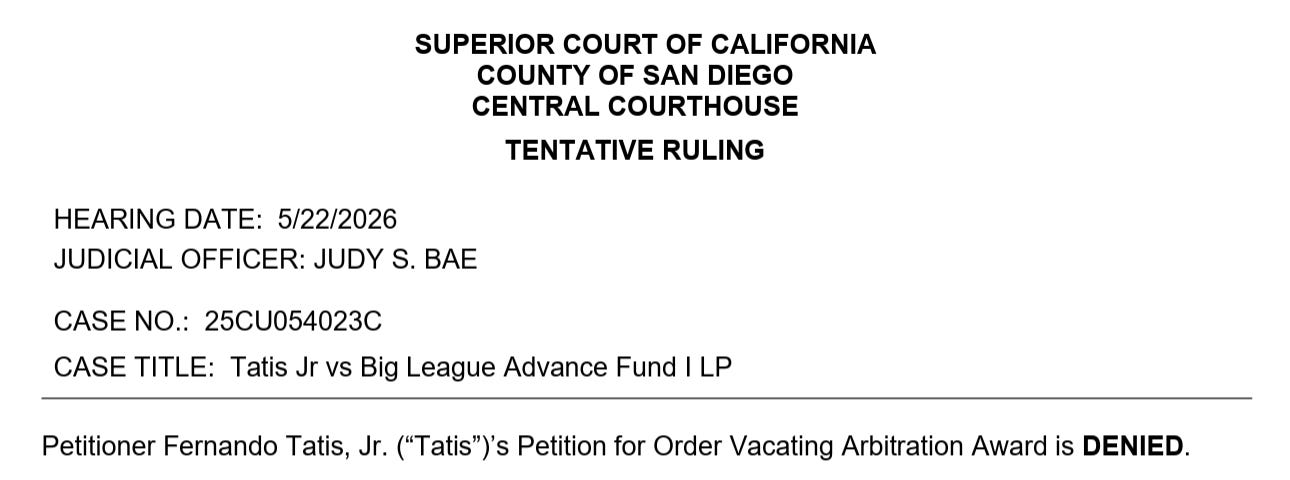

Last month, a San Diego Superior Court ruling showed how predatory lenders, financed and backed by Wall Street, are manipulating the limits of consumer protection among teenage athletes. At the center of the matter is Fernando Tatis Jr., a three-time Major League Baseball (MLB) All-Star and a two-time Gold Glove Award recipient, who now may be the hook for nearly $38 million.

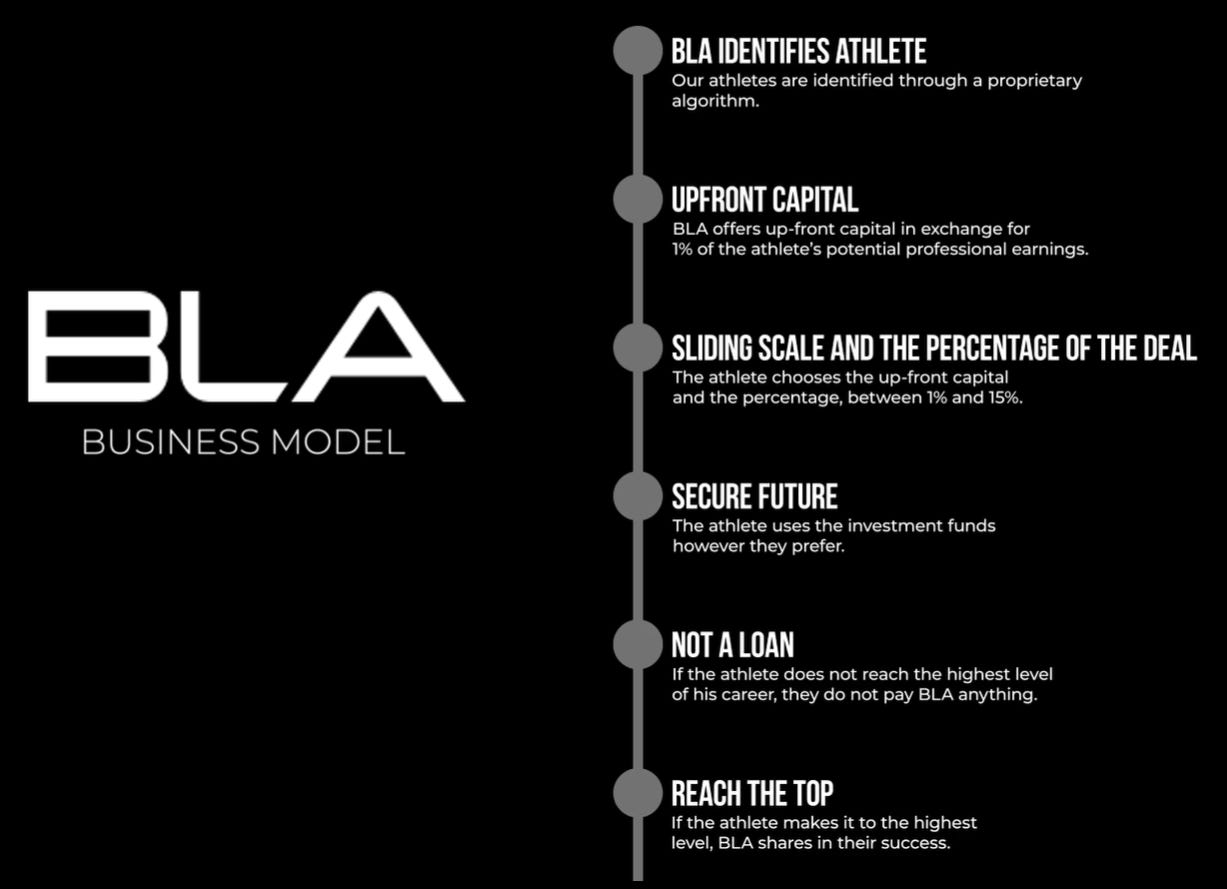

In 2017, Big League Advance (also known as Big League Advantage, but more on that later) approached a then-18-year-old Tatis Jr., who was living in the Dominican Republic and still learning English, and offered him $2 million in exchange for 10 percent of his future MLB earnings for 25 years. At the time, this little known, risky type of loan promised immediate financial security for a small portion of his earnings years later. Today, these loans are widely known as harmful, but cracking down on the firms that push these loans has yet to become a priority for regulators. Tatis Jr. was offered what is called an Income-Share Agreement (ISA) or an Income-Purchase Agreement (IPA).

Protect Borrowers has written about these kinds of nefarious loans in the past, but in the context of higher education. In the sports world, these contracts have exploded with minor league baseball players over the last decade, with the majority of players signing them coming from poor Latin American countries.

For minor league baseball players, ISA offers can be extremely appealing. On average, minor league players earned between $20,430 to $36,580 in 2025, making the temptation of these loans obvious. But Tatis Jr. alleges in a lawsuit against Big League Advance that they took even greater advantage of this situation, including: “deliberate failure to comply with California’s licensing requirements has allowed them to evade oversight,” “fail[ing] to adequately disclose the usurious interest rate which seeks to charge Plaintiff a 90% interest rate per annum over the course of his contract,“ and “misrepresent[ing] the agreement as an “investment” rather than a loan.” The contract was then presented to him as a take-it-or-leave-it offer, cutting his agent and lawyers out of the process.

You may wonder whether any judge ever looked at these terms or considered Tatis’s objections. Big League Advance includes mandatory arbitration provisions in its contracts with players, including Tatis Jr.’s. This allows the company to operate with little transparency or judicial oversight– instead relying on private arbitrators to adjudicate disputes over its contracts. The judge in Tatis Jr.’s case found that, based on California Supreme Court precedent, Tatis Jr. would have needed to file a challenge to the entirety of the contract before arbitration proceedings began. That ruling means that Tatis Jr. is required to follow an arbitrator’s October 2025 decision and owes Big League Advance $3.23 million, plus $240,515 in interest, $250,000 in attorneys’ fees, and $14,349 in other costs, totaling just under $3.74 million. Tatis Jr. also signed a 14-year, $340 million deal with the San Diego Padres in 2021, putting him on the hook to pay an additional $34 million. Over the life of his career, this would amount to more than 1,700 percent of the sum advanced in 2017.

Income-Share Agreements Are Predatory Loans Targeting Young Athletes

ISA lenders— many of which are funded by hedge funds, private equity, and wealthy individuals—deploy a business model that rests on the idea that these ISAs and IPAs are not loans. This hasn’t always been an easy argument for these firms to maintain. Just consider the name of the company Tatis Jr. is challenging: Big League Advance (emphasis added), a term that is synonymous with loans (oops!). When the company rebranded to “Big League Advantage” in 2022, Michael Schwimer, CEO and founder of Big League Advance, acknowledged that he was slow to realize this, saying “[t]hat’s how big of an idiot I am.”

Using advanced sports data and analytics, Big League Advance and other firms target hundreds of young players, mostly from Latin America, at the beginning of their careers who it believes could eventually land lucrative contracts in the big leagues. Like with other types of ISAs, this means treating individual players as a form of human capital and purchasing stock in them before the market sees their value (creepy!). Notably, these firms have access to data that the players themselves do not, and are able to make sophisticated offers to players based on this. While not all of these ISAs will work out, the firms only need to be correct a handful of times to recoup a massive return for their investors. At one point Schwimer and his investors even told HBO’s Real Sports Podcast they expect annual returns of at least 30 percent for 20 years.

And where other financial products have sometimes straddled the line of a consumer product or some other type of financial product, that distinction does not appear here. In Tatis Jr.’s lawsuit against Big League Advance, he alleges that the firm acknowledges that most of the players receiving them are using them for “personal, family, or household purposes,” including buying groceries, paying rent, or covering medical expenses of family members. The Washington Post found that one of the firm’s investment brochures filed with the Securities Exchange Commission claims this money lets players live in more “comfortable conditions.”

Firms like Big League Advance are offering contingent cash advances to young athletes for personal use, which are expected to be repaid with future earnings. But they are claiming that these are not loans, nor should they be subject to basic consumer protections. Nobody is obligated to play along with the industry’s fairy tales.

Big League Advance is Just the Tip of a Terrifying Iceberg

Big League Advance is just one of a number of investment firms peddling these sorts of cash advances to young athletes. Other companies include Nilly, Vestible, RockFence Capital, and X10 Capital. These investment firms are now also branching out from just minor league baseball players to college athletes, following the growth of the Name, Image, Likeness market. In another high profile case involving Big League Advance, Gervon Dexter, a former college football player at University of Florida sued the firm in 2023.

Dexter was in severe financial distress. He had taken out two high-interest auto loans that he could not afford, and was being threatened with collections. He had been evicted from his apartment after falling behind on rent. His girlfriend was expected to give birth any day, and his own father had just passed away.

That is when a Big League Advance agent messaged him on Facebook:

“We have a 6 figure financial/NIL opportunity for you. Would love to discuss more if you’re interested. Let me know what you think. 👊”

Eight days after the birth of his child, Big League Advance loaned $436,485 to Dexter in exchange for 15 percent pre-tax NFL earnings for 25 years. After he was drafted by the Chicago Bears, he signed a rookie contract worth $6,723,728. His 15 percent pre-tax lifetime debt to Big League Advance will amount to more than $1 million just from his initial NFL contract. Like Tatis Jr., if he is successful in the NFL and earns additional contracts, this figure will balloon because there is no cap on the maximum repayment of the loan.

We Already Have the Tools to Rein In This Harmful Industry

These sorts of financial arrangements are only able to persist because we have allowed industry to pretend that it is above the law. Lenders have claimed that their products are magically not loans so that they can purportedly skirt around a host of consumer protections, including by failing to become licensed lenders, by failing to comply with usury limits, and by engaging in abusive and deceptive practices. When athletes have sued these companies to escape these illegal arrangements, the firms have largely gotten away with these schemes by relying on arbitration provisions that kick the players out of court and lock them into lopsided, back-room negotiations—much like Tatis Jr. is currently experiencing.

The news about Tatis Jr.’s case led to many baseball fans wondering how an MLB superstar, and the son of a former professional player himself, could wind up in this situation. But he is hardly the only professional athlete caught up in such a predatory scheme. Big League Advance claims to have contracts with more than 700 players, including current MLB stars Elly De La Cruz, Jazz Chisholm Jr., and Keibert Ruiz, among many more. If loan sharks can take advantage of professional athletes, imagine what they will try to get away with when it comes to workers who lack the resources and connections these athletes have.

A decade after baseball’s ISA frenzy began, we are now seeing how this debt scheme is robbing thousands of players of their earnings simply because someone messaged them at a moment they knew the player was financially vulnerable.

For starters, state enforcement officials must treat ISAs and IPAs as loans and recognize that consumer protections already apply to them. As Protect Borrowers has highlighted previously, just because lenders don’t call ISAs loans does not mean they are not loans. For instance, in California, where Tatis Jr.’s lawsuit was filed, the state’s Department of Financial Protection and Innovation could review these lenders and their contract terms to ensure both are complying with state laws.

Many other states that are home to MLB teams have similar consumer protections. Public enforcers and regulators must step in to stop these scams because of the mandatory arbitration provisions that block players from pursuing justice in the courts. Thankfully, identifying where these scams are occurring is low-hanging fruit. These investment firms publish the names of the players under contract with them, and it is well known where the players live and work.

It doesn’t take a particularly savvy set of bad actors to peddle these products, which is why protections are necessary to bring these predatory ISAs to an end. This is a growing industry of predatory lenders who have access to a wealth of data about the likelihood that a prospect will succeed or fail, and on the other side of the negotiating table, you have a young adult with a dream and a need. That is why for every Tatis Jr. trapped in an ISA scheme, there are dozens more players that most fans have never heard of, who see their careers earnings siphoned away by these lenders. As Tatis Jr. said after the ruling last Friday: “I’m fighting this battle not just for myself but for everyone still chasing their dream and hoping to provide a better life for their family. I want to help protect those young players who don’t yet know how to protect themselves from these predatory lenders and illegal financial schemes -- kids’ focus should be on their passion for baseball, not dodging shady business deals.”

As Tatis Jr. continues to appeal his case and take on these predatory lenders in the courts, we need state enforcers to put an end to these scams before the next young player trying to pursue a childhood dream sees it become a financial nightmare.

Chris Hicks is a senior policy advisor at Protect Borrowers and a lifelong Kansas City Royals fan.

| A guest post by

|