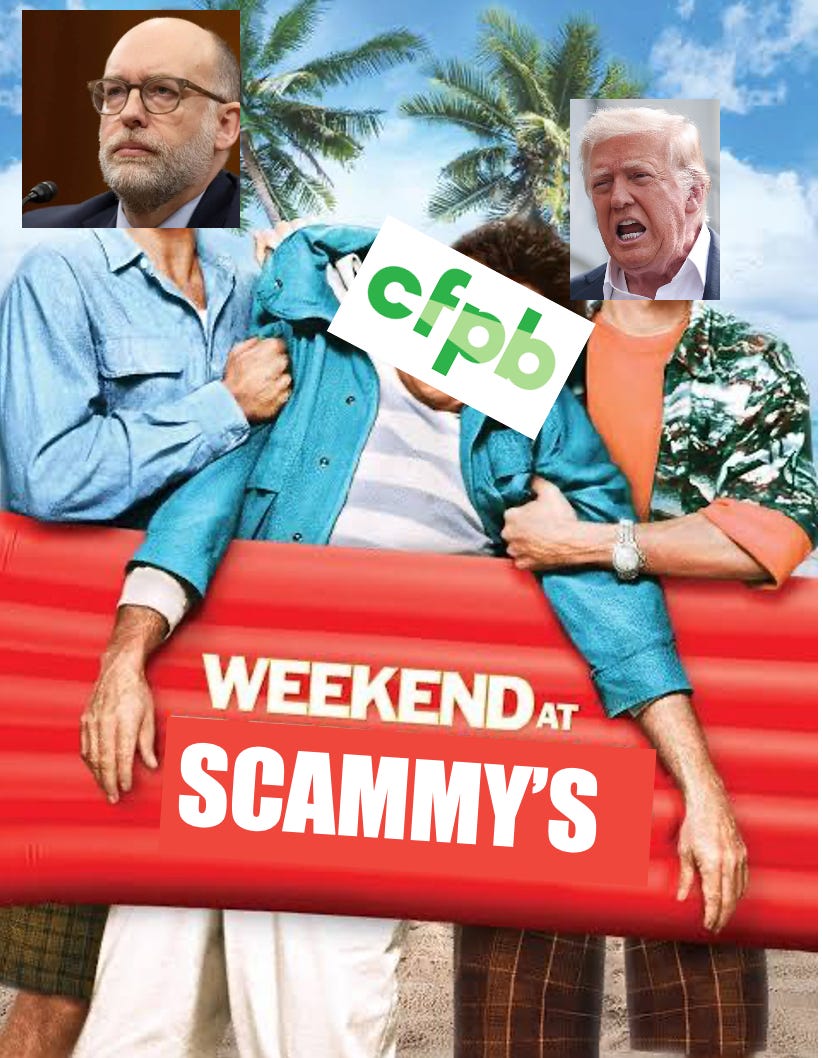

Cleanup on Aisle CFPB

The Bureau may be mostly dead, but it’s still the life of the party!

Depending on how you think about the current state of consumer financial protection in the Trump Administration, last week either brought a remarkable resurrection of the Consumer Financial Protection Bureau (CFPB) or showed us a sad new example of how Acting Director Russ Vought could prop up the corpse of the once-strong watchdog, “Weekend at Bernie’s”-style, to do special favors for companies caught in a whirlwind of scandal.

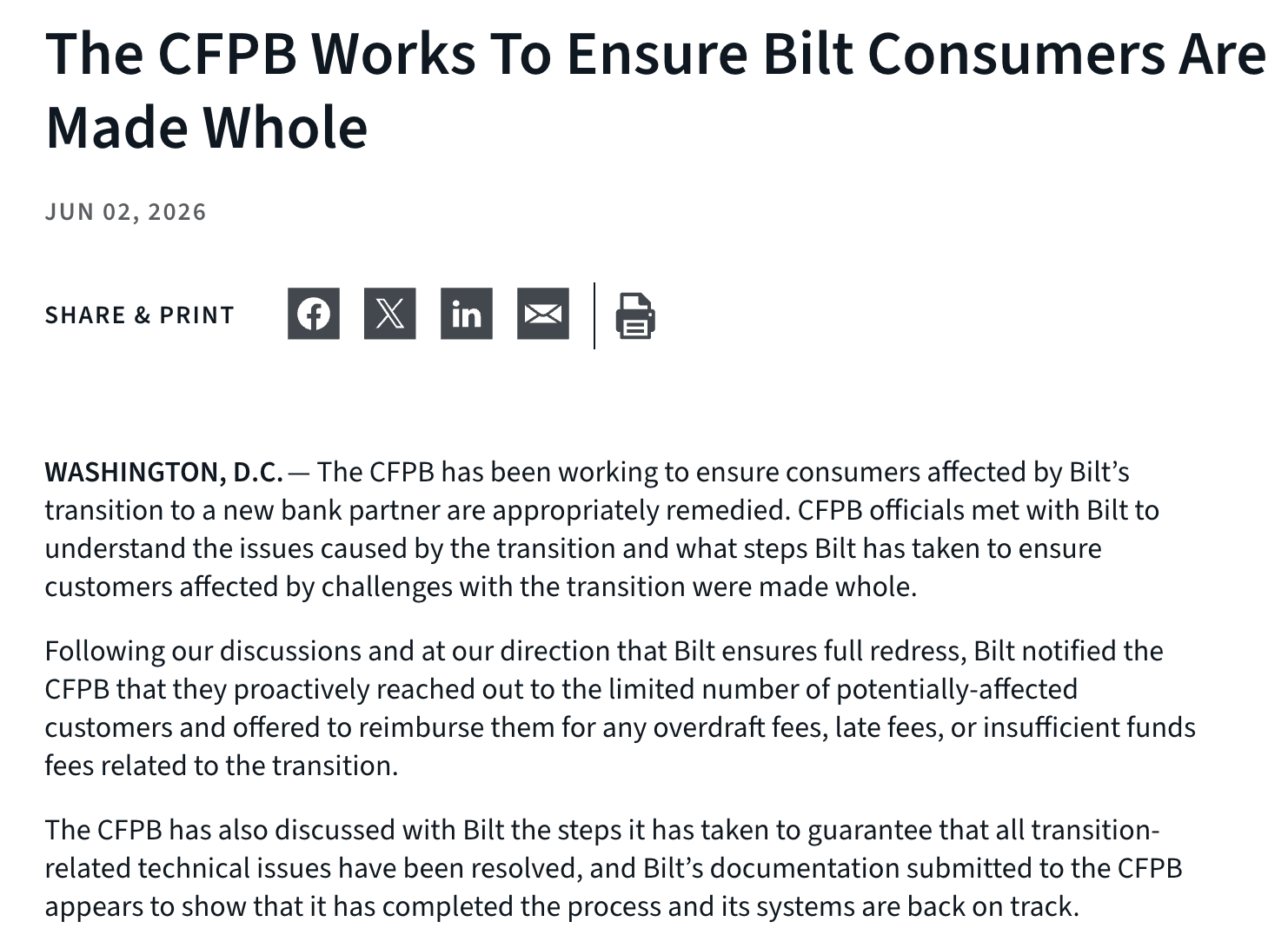

On Friday, CFPB issued a press release about the embattled “pay your rent and get points” fintech BILT. The timing and substance of this document is remarkable for a few reasons.

First, it was issued immediately following explosive reporting by a team at Bloomberg News documenting a MAGA secret handshake between Vought and a Republican lobbyist, Dennis Potter, who seemingly won an unprecedented corporate pardon for Toyota’s auto loan subsidiary, Toyota Motor Credit. The details of this are shocking, and include an extraordinary move by the consumer watchdog to halt payments from Toyota Motor Credit to its harmed customers—a restitution framework that the company had already agreed to make in a prior settlement, and at the behest of a Trump inauguration donor and its potentially unregistered lobbyist, who is an old Capitol Hill colleague of Vought’s. Even worse, as Bloomberg reported, Toyota’s lawyers actually scripted the language for the order releasing it from its obligations, and senior Trump leadership at the CFPB instructed staff attorneys to adopt it.

This is the stuff that drives Congressional oversight and brings down agency heads, at least in normal times. That’s all to say it’s understandable that the Trump CFPB brass would want to show that the agency can do vaguely “consumer protection-y” things at this moment in time in particular.

Second, it comes as reports indicate that CFPB is slowly being brought back to life, but to ramp up prosecutions of financial firms that help communities that Trump wants to hurt. As Andrew Ackerman at The Washington Post reported earlier this week: “A year in, a much smaller bureau is still standing and has been remade to advance the president’s political goals.”

Ackerman’s reporting builds on a piece by my colleague Allison Preiss, explaining that the Trump team has more or less thrown in the towel on the effort to “delete CFPB.” This report also adds to a set of reporting on other ways the bureau is being used to punish enemies and reward allies. As I told Bloomberg’s J.J. McCorvey earlier this week in a story about pressure on banks to constrict lending to undocumented people, there is a very aggressive culture war being waged through this White House, and now it has come for Wall Street.

Third, the CFPB made this announcement a few days before the White House announced that it had nominated Capital One executive and former Trump 1.0-era CFPB deputy director Brian Johnson to lead the agency. If you’re thinking about setting up your guy to weather an ugly confirmation hearing, having some stuff to point to that shows the agency is still alive and kicking is politically useful.

Is BILT a pawn or a player?

In BILT, we have a company that messed up badly. Customers’ money seemingly went missing, was eventually found, and the company claims to have learned from its mistakes and made amends. Its problems drew scrutiny from advocates, including us. It also drew oversight from Senate Banking Committee Ranking Member Elizabeth Warren, resulting in boldfaced coverage in the Wall Street Journal.

Five days after the Journal piece, CFPB emerged to assure the public that everything is OK at BILT. This is unprecedented. For those of you not steeped in CFPB mechanics, there are two ways for a company to resolve issues in partnership with the agency. First, the CFPB can use supervision to monitor an effort to remedy mistakes—this is, in regulator-speak, “non-adversarial.” It is also confidential, so companies trade an assurance that the agency is satisfied with their remedy for an agreement that the agency cannot publicize the outcome. Alternatively, CFPB can bring a public enforcement action against a company, which can either end in a public settlement or a lawsuit and a judgment. A typical CFPB settlement has a clear statement of the laws violated, the steps a company is taking to remediate unlawful practices, and oftentimes, the number of people affected. CFPB, when it functioned, routinely did both of these things—but lately, not so much.

BILT didn’t get either of these deals. We do not know what laws CFPB alleges BILT violated and we do not know how many people suffered the consequences when the company rushed ahead with the rollout of its new cards. Its coordination with the agency was publicized by the CFPB, which gave it a seal of approval in a press release without fulfilling its obligation to the public to explain what happened behind the scenes. In brief, it was not the subject of confidential supervision or the target of a public enforcement action, at least according to this release. Instead, it has its primary federal regulator on record saying “nothing to see here,” without any assurances that the law was followed either substantively or procedurally.

This is a terrible outcome if you care about protecting consumers or preventing corruption. It is also a giant “open for business” sign to any lobbyist, MAGA grifter, or bank executive who wants to cut a deal with the CFPB to fend off oversight, private litigation, or worse. It’s also bad for a free market and for honest businesses who don’t want to depend on special favors from the government to be able to compete.

New leadership, same corruption

This piece was mostly written before news of Johnson’s nomination broke last night. Tapping a Capital One executive for this post is a bad sign for any number of reasons, but particularly because Johnson’s current employer was the recipient of a corporate pardon from Russ Vought last year. In early 2025, the CFPB alleged that Capital One cheated its customers out of more than $2 billion in interest payments on savings accounts, but the Trump CFPB dropped the case permanently a few months later. Curiously, however, Capital One soon thereafter reached a $425 million settlement in a class action involving virtually the exact same allegations! Certainly, if the Senate moves forward with a confirmation hearing for Johnson, the role of his involvement—if any—with this massive corporate giveaway will need to come to light.

This will be Johnson’s second pass through the revolving door, having served as CFPB Director Kathy Kraninger’s deputy and deregulatory hatchet man during the first Trump Administration. This is just another piece of evidence in the increasingly strong case that Trump will use CFPB to punish his enemies and reward his friends—it’s already happening everywhere you look.

ed. Note. This post is not really about the state of play at BILT. For our past coverage on the BILT mess, see here. We also asked Bilt if they wanted to offer a comment on this story and they provided the following, which we are publishing in full:

“Our members have been our priority since day one. While the transition to the Bilt Card 2.0 in February represents an even more exciting future that offers our membership richer rewards and greater flexibility, the transition also attracted unexpectedly high demand, and some of our members experienced gaps in service that are simply unacceptable to us.

In response, we increased our customer service capabilities to address this and proactively communicated with any impacted members. All outstanding issues relating to the card transition in February have been addressed and resolved.

Should any member ever have an issue we encourage them to contact Bilt, as we will do everything we can to make it right.”

Mike Pierce is the executive director of Protect Borrowers.

Just what we need, Citibank in charge of the CFPB! Hello wolf, let me give you the keys to the henhouse!