This Week In Debt: 3/2/2026

Mr. Beast peddling kiddie EWA loans, MCA lenders played themselves, and worse!

Morning,

Welp, it looks like the YouTube celebrity Mr. Beast owns a fintech app targeting kids with Earned Wage Advance (EWA) loans, risky stock trading, and other goodies.

I did a thing the other week about the Kardashian Kard, a Kardashian-linked debit card from 2010 that drew essentially universal criticism for targeting teens and having bad fees. That pressure killed the Kard, but the intersection of youth, celebrity, and retail finance never dies:

Mr. Beast is a person who is big on the internet, particularly on YouTube. (He is also big in reality—the internet tells me he is now a billionaire). I have mostly succeed in not learning or thinking at all about Mr. Beast, except that I once opined that I don’t like the name of his line of chocolates.

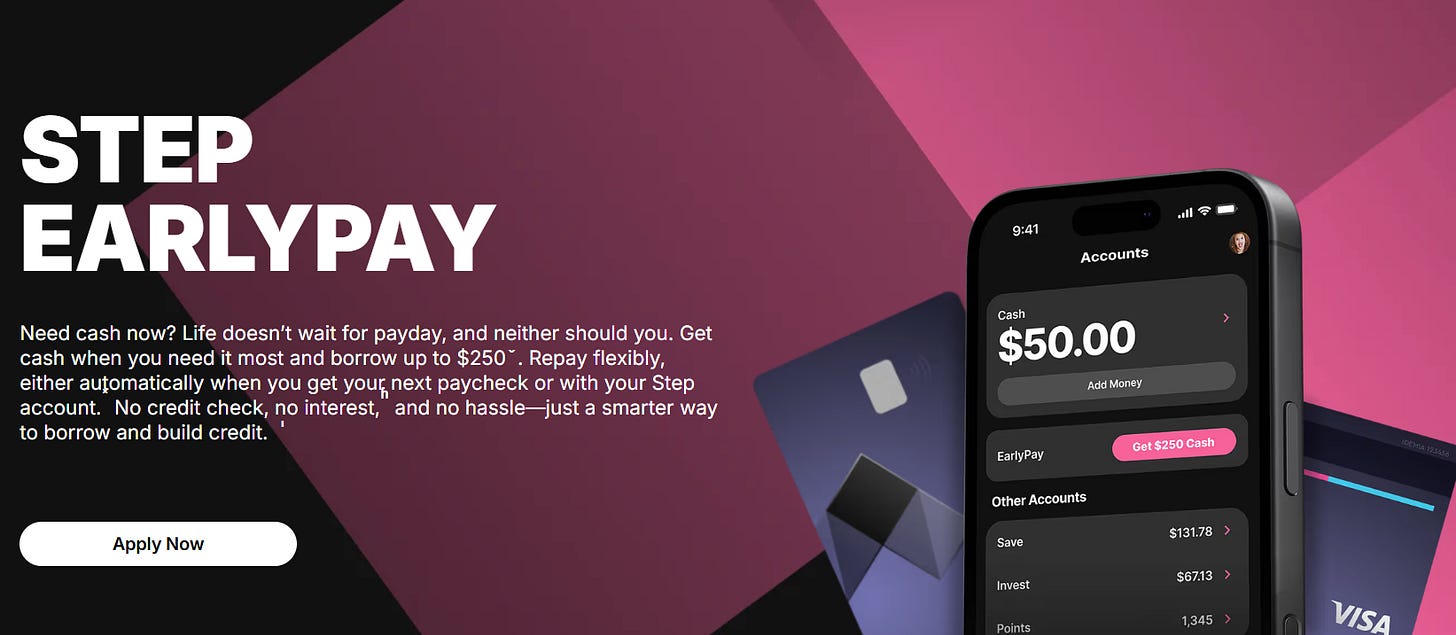

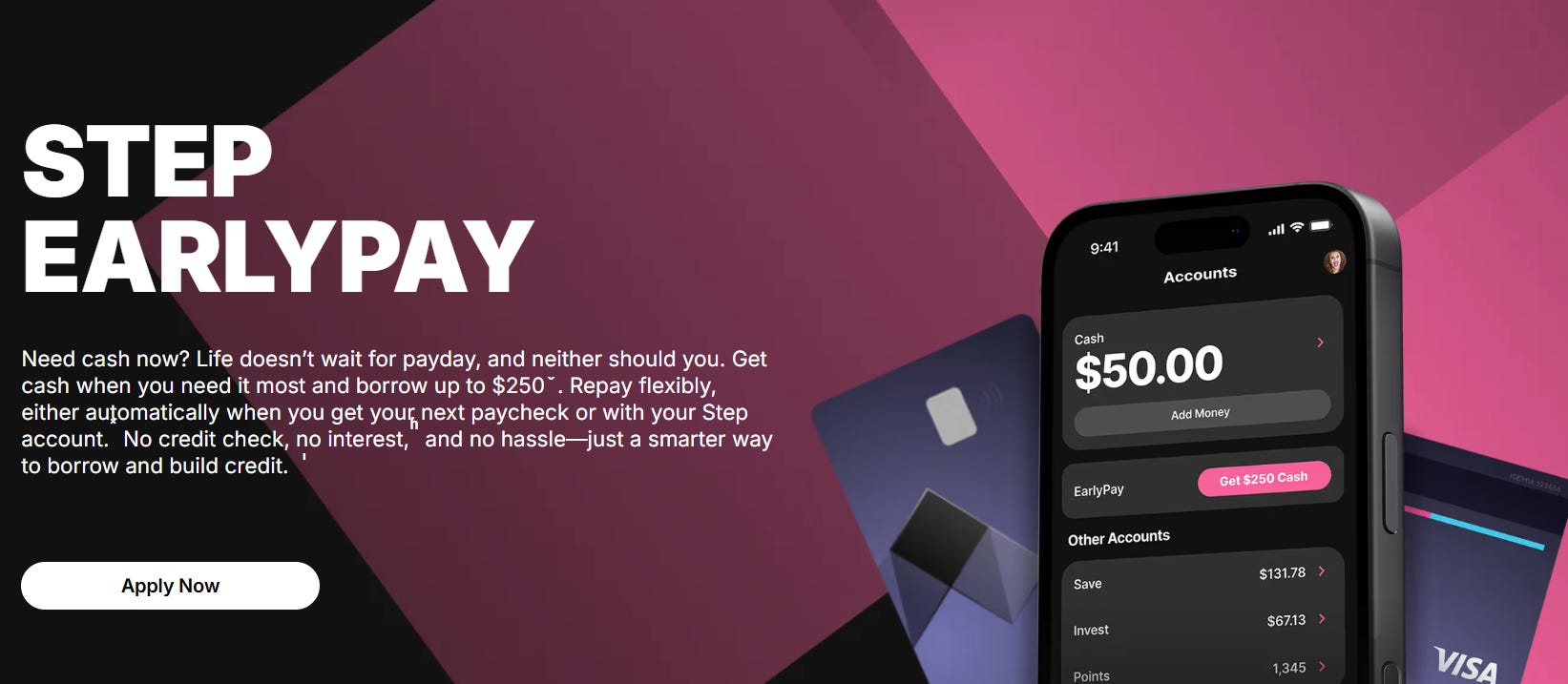

Step, meanwhile, is a sort of financial everything app that does not have an age minimum. And to cut to the chase, here are some of its features:

There’s a built-in kiddie earned wage advance product (recall: EWA loans are payday loans with better websites):

Uhhhhhh.

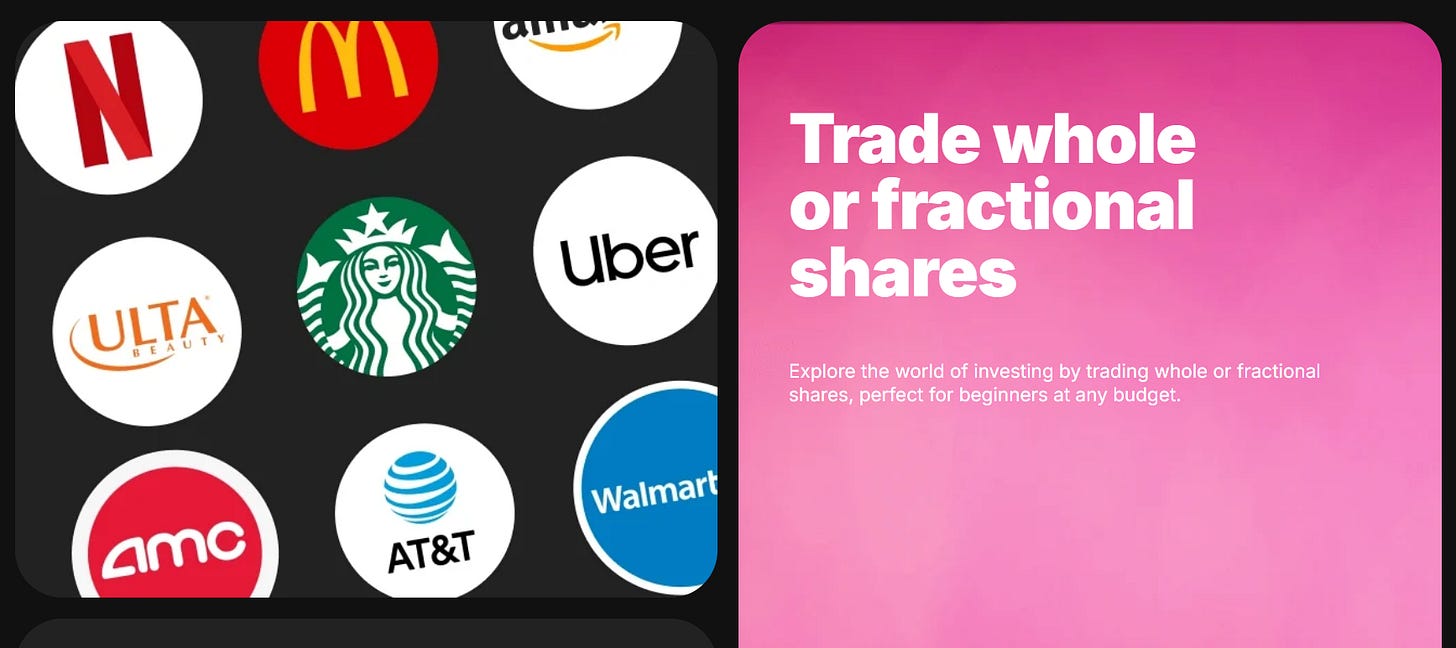

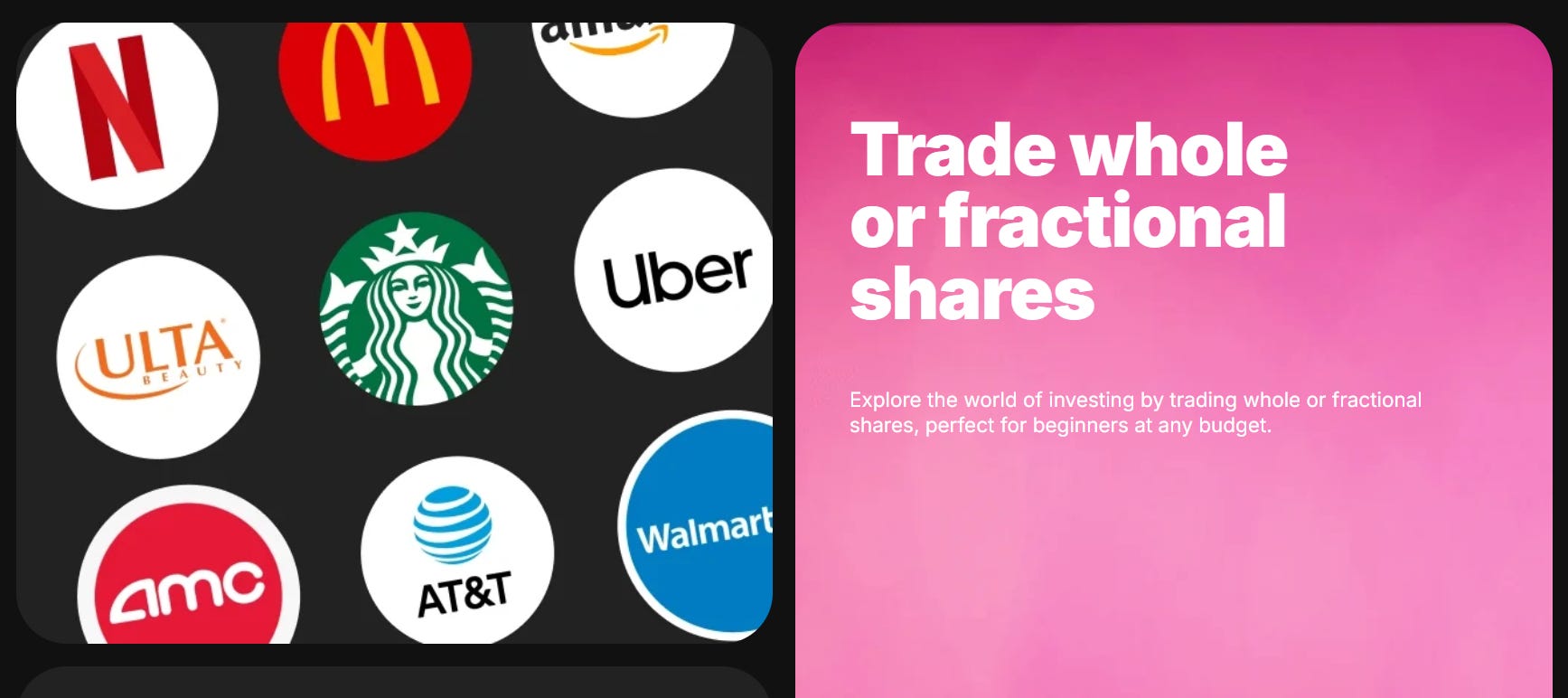

There’s also a built-in brokerage that lets kids trade fractional shares of single-name stocks:

You need parental consent on this until you’re 18 but to reiterate uhhhhh!!

There are other features, too. There’s an app, and you get a Visa card linked to a bank account provided by Evolve. You can go use that card on youthful follies, or whatever. “There are no monthly, overdraft, minimum, or account management fees,” but there are fees on “adding funds [in an amount] below $20” and various other things. (Step says it’s making money mostly on interchange.)

If you get their premium level (“Step Black”) by setting up a monthly direct deposit of $500 or more, or by paying $4.99 a month, you can get 3 percent interest on your savings and rewards that, per the Step website, appear to involve video games and ice cream. (It also appears that if you get Step Black you can get a fun black credit card that you can use to stunt on your presumably middle or high school-aged friends, though to be fair adults do that to their adult-aged friends too.)

If this smells to you like the candy-flavored vapes of the 2010s, you’re in good company.

Maybe this is one of Mr. Beast’s famous social experiments? Either way, it seemed like the business model of “bank-partnered financial everything app geared toward a specific population that makes money on interchange” had sort of broadly died (e.g.). But maybe it’ll return just in time to target kids.

Elsewhere: New York AG sues Valve, alleging ‘loot boxes’ [in video games] promote illegal gambling.

Ok, ok, enough of the youths. Below, I have gathered the best of the internet from the past week on our worthy topic of consumer finance. Scroll to your heart’s delight.

So without further ado . . .

This Week In Debt for 3/2/2026:

Business payday lenders hoisted themselves by their own petard? Say you were an evil loan shark to small businesses. You’d want to charge really high interest rates. That’s your whole thing! But if you charge rates that are too high, the small businesses will just go bankrupt, and you might not get anything back. (For this hypo, ignore the possibility of sending Chris Moltisanti to collect.)

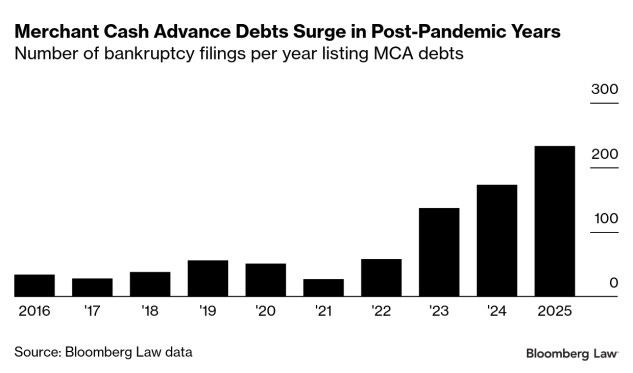

A story in Bloomberg Law this week rang the alarm on how “merchant cash advance” (MCA) loans, which are just payday lenders for businesses, appear to be increasingly pushing small businesses toward bankruptcy. That’s very bad.

But I submit to you that this is also a story about how MCA lenders have overplayed their hand by both turning the dial too far toward “high rates” for their own good and seeing certain bankruptcy-related Plan B’s get crushed by the weight of reality:

Merchant cash advance funders are increasingly being listed as major creditors when small and even midsize companies file for bankruptcy, highlighting a surge of activity in a largely unregulated area of alternative business financing.

That graph is ugly, and the article paints a picture of MCA lenders being extremely predatory. (E.g., “When Rogers Landworks LLC filed for Chapter 11 in December, the Florida-based land clearing and trucking company told the court that its bankruptcy ‘was necessitated by accumulated MCA debt and aggressive MCA collection activity.’”) On some level, the real story here is that MCA lenders are targeting companies that should have probably just filed for bankruptcy in the first place. (Not just my view! From a lawyer in the article: “I’m loath to think of an instance when bankruptcy isn’t the best solution for a debtor who has multiple merchant cash advance loans.” That comes right after she said: “And nobody has just one. They all have multiple.”)

But this status quo may not even help the MCAs! You see, the MCA companies have seemed to think they have a get-their-money-even-if-the-company-you-lent-to-is-bankrupt card. That card consists of arguing that MCA companies aren’t lending to small businesses so much as buying those businesses’ future revenues at a discount. MCA companies make this argument because while debts get discharged in bankruptcy, sales might not. But the MCA companies are increasingly losing on this argument and having their precious loans disappear!

In an October ruling in the US Bankruptcy Court for the Middle District of Florida, Judge Tiffany Geyer approved an Orlando-area fertility clinic’s restructuring plan that discharged MCA obligations. She ruled that the debts cere incurred more like loans than purchase agreements and the clinic didn’t have property interests to convey in future revenues.

“There’s a lot of caselaw that recategorizes them as loans, but it’s not universal or automatic,” said Ohio-based bankruptcy attorney Patricia Fugée of FisherBroyles LLP. “I think MCA funders are losing on the sale versus loan argument more often than they’re winning.”

It seems, then, like there are at least four (not necessarily mutually exclusive) paths forward for the MCA industry:

MCA lenders continue charging sky-high (and now possibly even sky-higher) rates with an eye toward gambling on a favorable ruling in bankruptcy when it arises, noting that those rulings do happen;

MCA lenders ramp up the aggressiveness of their efforts to keep the companies they’ve lent to out of bankruptcy court until they (the lender) have been paid, either via shades of illegality (see Moltisanti, supra) or with something like new avenues for loan modifications (hey that could be nice!);

MCA lenders trend toward lowering their rates upon recognition that prevailing rates are counterproductively pushing businesses into bankruptcies that could otherwise maybe be avoidable (ha wishful); and

The MCA business model just sort of falls apart.

Expect more development in this space! In the mean time, it’s nice to see courts call a loan a loan.

Everybody wants to be a bank, part 48856568. A theme I come back to is that industry complained for years that the big evil regulatory post-Crisis regulatory apparatus had allegedly made it so lame and costly to become a bank that nobody would want to become a bank, but now everyone wants to be a bank. In just the last week, we saw Payoneer, Crypto.com, Morgan Stanley, Edward Jones, and others became or attempt to become a bank. And now we have headlines like this:

Things are so busy in bank applications that the OCC is having to pull staff in from elsewhere to do “one- to two-year rotations within the chartering arm.”

Of course, a lot of this has to do with companies wanting to do crypto custody stuff and/or issue stablecoins. And a lot of it also has to do with the ongoing dismantling of that regulatory apparatus I mentioned above.

But like . . . a lot of it isn’t about crypto, and it remains obviously the case that the regulatory situation could change again in fewer than 3 years. You know my take: what’s really up here is that at the end of the day, “people/companies fundamentally want to be banks and do bank-like things,” regardless of whether industry advocates tell them they should want that.

Elsewhere, from the National Consumer Law Center: New Predatory 100% APR Bank Seeks Trump Administration’s Approval (emphasis added):

The Office of the Comptroller of the Currency (OCC) should deny the application of Enova International, the owner of CashNetUSA and NetCredit, to become a national bank, advocates urged in comments submitted Friday to the OCC. If Enova were allowed to become a national bank, it would be able to offer its 100% to 300% APR loans across the country, ignoring state laws nationwide.

The Trumps are (likely) going after fair lending: One problem that the Trumps have had in trying to kill the Consumer Financial Protection Bureau (CFPB) is that the consumer finance industry actually relies on the Bureau in a lot of ways. E.g., the CFPB is the thing that companies turn to so that they can make sure they’re complying with existing rules around data disclosure for fair lending compliance.

As a solution in their quest to kill the Bureau, the Trumps seem to be trying to kill the ways in which companies rely on the agency. To the fair lending data disclosure point (this is all taken from a LinkedIn post by Elena Grigera Babinecz):

What’s going on here is that in December the CFPB put out a notice saying it wanted to get the public’s comments on a potential reconsideration of what kinds of data companies have to report under the Home Mortgage Disclosure Act (HMDA), a key fair lending law. Then, in early February, a really really conservative group called America First Legal (AFL) wrote in to say that the CFPB should just entirely rescind Regulation C, which is the regulation that implements HMDA for fair lending purposes. A rescission like that would basically mean killing HMDA’s fair lending data collection protections.

A flavor of AFL’s attitude about this whole thing (emphasis added):

“Regulation C turns mortgage applications into a government-mandated demographic sorting exercise,” said Alice Kass, Attorney at America First Legal. “These policies exceed the CFPB’s authority and compel the collection of protected personal information without legal justification. OIRA must exercise its authority and revoke its approval of this unlawful data collection.”

And then last week the CFPB announced it was extending the period during which it would allow comments on its potential reconsideration of the HMDA data collection rules. Some folks are reading the tea leaves here to mean that the Bureau is going to take AFL’s advice and neuter HMDA. Folks have until March 26 to comment, so for all you consumer advocates reading this—it is, indeed, time for strongly worded letters.

Elsewhere:

New Fed working paper from Matthew Maury (hi, Matt!), Michael Suher, and Jeffery Y. Zhang: Enforcing Fair Lending: Evidence from Mortgage Market Litigation (emphasis added):

Does fair lending litigation impact mortgage lender decisions? Using a novel dataset of all fair lending legal actions from 1991 to 2023, we find that it does. In the wake of legal settlements for discrimination against Black borrowers, lenders significantly reduced denial rates for Black applicants. The reductions offset pre-litigation racial disparities in denial rates by litigated banks, relative to those banks’ competitors. Origination rates for Black applicants also increased post-litigation. We further observe evidence of a spillover effect on the approval decisions of non-litigated banks operating in the same city as a litigated bank. Altogether, the evidence suggests that the enforcement of fair lending laws is an effective tool to reduce racial discrimination in credit markets.

American Banker: Judges seem inclined to allow CFPB RIFs — if there’s a plan

A mixed news bag in the states:

Good news: New York releases draft regs for Buy Now, Pay Later. A summary from the press release:

The regulations published today will implement that law by:

Establishing a licensing and supervision framework for any entities engaged in Buy Now, Pay Later activity in New York;

Prohibiting excessive fees, including convenience charges, and limiting late fees and other types of penalty fees;

Requiring lenders to make clear to New Yorkers if loans will be reported to credit reporting agencies;

Establishing rules for timely resolution of consumer disputes; and

Protecting consumer data from misuse or exploitation.

Bad news: A bad rent-a-bank opinion in California may greenlight certain predatory loans, at least for now. The case is sort of fact-specific, but basically a California court held that the company OppFi, which makes high-interest loans in CA and elsewhere through a bank in Utah, had successfully structured its lending in a way that magically brough those loans outside of California’s usury laws.

A great new report from Michael Best and Carolyn Carter at the National Consumer Law Center takes on the phenomenon of debt collectors harmfully garnishing financially strapped people’s bank accounts, and details how states can fix it (and my god I love their graphics department, also emphasis added below):

The sad piggy bank! As debt collection lawsuits surge to pre-pandemic highs, more and more families will see their cash and property seized by debt collectors. All states protect some of a family’s property from seizure by debt collectors to enforce a court ruling for a debt, but in some states the protection is minimal or is so difficult to claim that it is essentially a dead letter.

Protecting a basic amount in a bank account is particularly important. Most wages are direct-deposited, so allowing a debt collector to seize a family’s bank account means seizure of the breadwinner’s paycheck that the family was relying on to pay for rent, food, transportation to work, and utility bills. It also means that all the family’s outstanding checks and debits are likely to bounce. No family should be made homeless or destitute because of an old credit card debt.

Higher education/student loan grab bag!

From Jordan Nellums, Amber Villalobos, and Denise A. Smith at the Century Foundation: Many States Are Shortchanging the Students Most In Need of Aid—Including Students at HBCUs. The result is that a lot of state grant-based financial aid is going exactly where it’s least needed, and vice versa.

As part of their efforts to dismantle the Department of Education (ED), the Trumps are handing more of ED’s responsibilities to other agencies (good summary here):

“As we continue to break up the federal education bureaucracy and return education to the states, our new partnerships with the State Department and HHS represent a practical step toward greater efficiency, stronger coordination, and meaningful improvement,” said U.S. Secretary of Education Linda McMahon.

It’s sort of like those videos where small children don’t understand that when you pour water into a differently shaped vessel, the amount of water doesn’t change. Moving bureaucratic responsibilities from ED to somewhere else doesn’t eliminate them! And those moves probably makes it only more likely that those responsibilities will be badly executed!

Hopefully the Trumps don’t make progress advancing along Piaget’s stages of cognitive development before 2029.

HUGE props to the Project on Predatory Student Lending, which in one week beat both a Department of Education effort to delay relief for defrauded borrowers and an attempt at the Supreme Court by certain for-profit schools to block those borrowers’ loan discharges.

ED Warns Colleges With High Student Loan Nonrepayment Rates (emphasis added):

At least 25 percent of borrowers at more than 1,800 colleges and universities are behind on repaying their student loans, according to federal data released last week that offers more insights into the growing delinquency and default crisis.

How’s private credit/equity doing?

Boaz Weinstein Warns ‘Wheels Coming Off’ Private Credit Funds.

Private Equity’s Dry Spell Worse Than 2008 Crisis, Bain Says.

Private Credit Fund Is Selling $477 Million of Assets at 94% Value as Industry Worries Continue.

Apollo Private Credit Fund Marks Down Portfolio on Soured Loans.

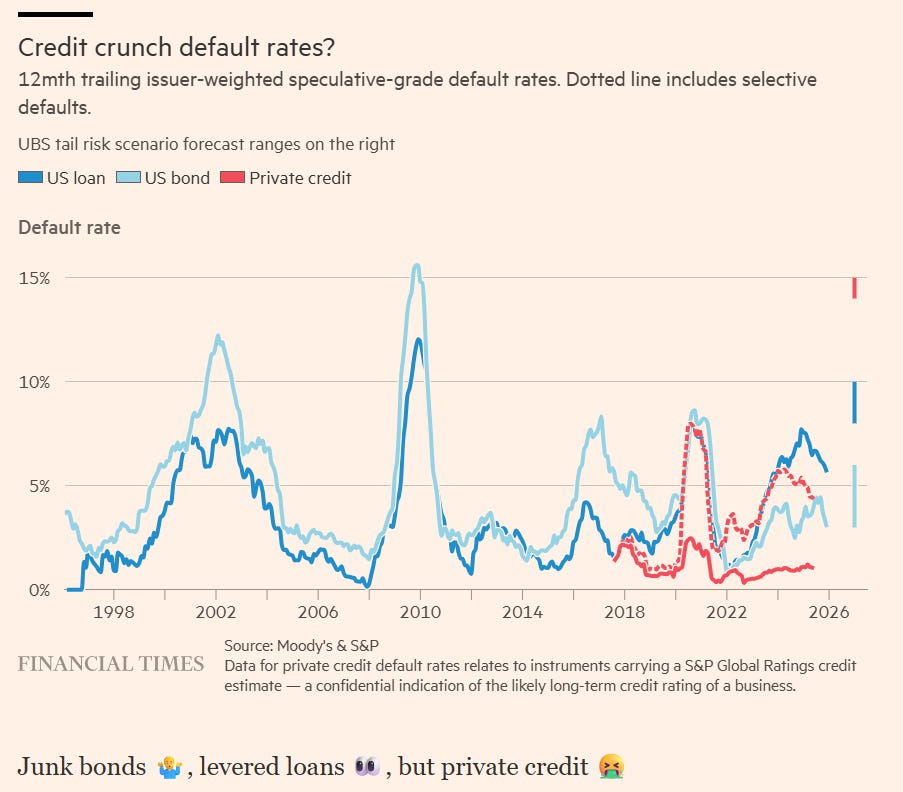

The FT reports on a research note from UBS credit strategies about defaults in corporate credit (emphasis added):

These are big global financial crisis-like — or at least dotcom-bust-like — numbers. While we haven’t spotted a time horizon for the forecast, we’ve whacked them onto this chart of historic default rates to give you a sense as to where they sit versus the last couple of decades’ experience:

Their dataset isn’t continuous, but notice the jump at the end.

In London, we have yet another private credit blowup involving possible fraud.

Also: a very good primer on what people mean when they say PE is bad for society, written by an anonymous “senior partner” at a “leading” law firm that presumably does a lot of PE work: The Dark Side of Private Equity.

And finally, some potpourri:

[California] Attorney General Bonta Exposes Amazon Price Fixing Scheme Driving Up Costs for Americans, Asks Court to Immediately Halt Illegal Conduct.

Fifth Circuit Holds the Telephone Consumer Protection Act Does Not Require Prior Express Written Consent for Telemarketing Calls.

Politico: Wall Street lawyer to head Federal Reserve department of supervision.

WSJ: Americans Are Leaving the U.S. in Record Numbers:

Last year, more Americans moved to Germany than Germans moved to America. The same was true in Ireland, which welcomed 10,000 people from the U.S. in 2025, about double those who came in 2024.

Binance Employees Find $1.7 Billion in Crypto Was Sent to Iranian Entities.

In New York, ,the mega-wealthy are getting tax breaks by converting multifamily housing into “mega-mansions.”

Nelnet’s 2025 earnings hit this week. Nelnet is a student loan servicer. I bring this up mostly because they are a freaky little oddity in the student loan space in a way that I found amusing. I.e., from their 10-K compare:

The Company was formed as a Nebraska corporation in 1978 to service federal student loans for two local banks.

With (emphasis added):

The Company has also broadened its operating business mix both within and beyond its historical education-focused activities. These businesses include banking and other financial services conducted through the Company’s bank and other subsidiaries, asset management and related customer-facing servicing, real estate development and management, reinsurance operations, renewable energy development, and selected strategic interests in early-stage, emerging growth, and other operating enterprises [i.e. venture capital].

They also are buying up to $26 billion in BNPL loans from Klarna? What a silly little object.

WSJ: Raves, Debt and Deaths: How a Wall Streeter Came to Own New York’s Biggest Club:

“We are left to absorb the cost of high-risk speculation by investors and financiers,” said Jon Mammele, a construction manager on the Mirage’s renovation whose firm is owed $248,650 by the venue.

The Verge: Burger King will use AI to check if employees say ‘please’ and ‘thank you’ (but also, and you do in fact have to give it to them on this, they named the AI bot “Patty.”)

The Style Section:

Proposed Guadí skyscraper for New York. (Another rendering.)

Incredible Cincinnati “mushroom house.”

Italian foreign exchange student tries, enjoys Olive Garden. Also: Red Lobster’s turnaround appears to be succeeding.

Here’s a picture of Kendrick Lamar and his wife on the Revenge of The Mummy ride at Universal Studios.

Have a great week!

| A guest post by

|