This Week In Debt: 2/23/2026

With enemies like these . . . rhetoric, student loan defaults, inquoracy, and more!

Hi,

A thing I talk about a lot is that the industry advocates in the consumer finance world are surprisingly bad at advocacy. I lived in DC for a while; I love a hacky argument! But just in terms of wielding the artform, industry types in consumer land lack the sauce more frequently than you might expect.

(If that sounds extremely bitchy of me, and it might, then rest assured that the industry types still win a lot, which is obviously what actually matters. After all, they have money!)

Industry’s lacking rhetorical prowess came to a head last week when the deregulatory industrial complex decided all at once that it’s bad that states are trying to pick up where the federal government has fallen off when it comes to consumer protection. Three examples:

In Open Banker, a fintech guy complains that states stepping in on data privacy, crypto, AI, etc amounts to a problematic “Balkanization.” But he sort of concedes that he knows his argument is bad? Or he can’t really figure out what his argument is? E.g., he says about data privacy regulation (emphasis added):

The net result of the federal government ceding the privacy playing field to the states has been to create a highest common denominator problem, where the most restrictive state law dictates the national compliance baseline, effectively allowing state legislatures to set national policy. But the longer this approach is allowed to continue unabated, the larger the discord among states’ respective data privacy requirements is likely to become, leading to a reality in which companies that wish to offer their products and services in the United States will be required to comply with 50 distinct state laws.

Wait, wait, is the problem that the companies will just set their policies to match the most restrictive state (“highest common denominator”), or is it that companies will have to comply differently (“discord”) in every state? He doesn’t really say, and then he concedes that “‘compliance burden’ is a frequent and ineffective policy argument,” so I hope it isn’t one of the arguments he’s making.

The author then goes on to argue that states should not be able to protect consumers because doing so could make U.S. markets less competitive than those abroad, particularly in China. (You can read the quote here if you want.) I mean, surely “yeah this is bad but if you don’t let us do it then China wins” is where argumentation goes to die.

It’s just a little too obviously unavailing. No sauce.

In Consumer Finance Monitor, the folks at Ballard Spahr (a law firm that represents a lot of consumer finance companies) are mad that states are going after shady rent-a-bank deals. At issue here is a recent court ruling (detail here) more or less saying that states can, in fact, put caps on the interest rates that banks charge people in their state even when those banks happen to be based in a different state. In response, conservative Senators introduced a bill to overturn the court ruling. And here is how Ballard Spahr described the situation (emphasis added):

If the Tenth Circuit’s panel decision stands and is replicated elsewhere, other states could pursue similar strategies. Conversely, if Congress enacts the American Lending Fairness Act, it would reaffirm a uniform federal standard for interstate rate exportation and significantly curtail the ability of states to extend their usury laws beyond their borders.

Oh come ooooon. You would have me believe that when State A says that banks in State B can’t make loans in State A that are already illegal in State A, that action amounts to State A “extend[ing] their usury laws beyond their borders”? This argument is sort of both too wrong to be cute and not wrong enough to be admirably brazen. Back to work, guys.

Elsewhere: Oregon is taking steps to go after rent-a-bank deals.

You probably saw this already if you read this Substack, and this item is not about state stuff, but either way: the White House Council of Economic Advisors (CEA) produced an estimate that the Consumer Financial Protection Bureau has cost consumers ~$369 billion by increasing the cost of credit through regulation, then got absolutely clowned on for the low quality of its advocacy math. (E.g., e.g.) Someone asked me if I was going to do like an Epic Takedown of the CEA report, but it’s sort of too dumb to require one (though Adam Levitin has a pretty definitive debunking over at Credit Slips).

To highlight one particularly funny aspect of the report, though: check out how the CEA estimated the “cost” of the CFPB’s work in auto loan and credit card markets. To do that, the CEA first estimated how much the CFPB had purportedly cost consumers in the mortgage space (and, as Levitin details, they did so in a way that is basically indefensible). Then, as Levitin summarizes (emphasis added):

Having concluded that the CFPB is somehow responsible for $116-$183 billion in additional borrower mortgage costs, the CEA then extrapolates from that to increased auto and credit card lending costs. How? By comparing the number of complaints per dollar of loan volume across credit products. In other words, figure out the complaint rate for mortgages, for auto loans, and for credit cards, and assume that if there were 5x as many complaints about credit cards as for mortgages, that the regulatory cost would be 5x as large. This is one of the most asinine analytical moves I’ve ever seen.

Again, you almost have to respect how brazen it is, but it’s just too facially dumb to even be effective advocacy.

There are more substantive points that I could make here, including but not limited to:

It seems like these people sort of just hate democracy?

I regularly travel between states, and I have not found it hard to comply with the subtle ways in which their laws may differ.

What if we make a deal where you have to comply with the law and in return you get limited liability and the other almost innumerable benefits that flow from using the corporate form (ha no this is the deal we already made).

But for today I will just focus on the rhetoric. Be better hacks!!! Isn’t that what they pay you for?

Alright, enough. Onto the links. Below, I have once again brought you the best in the week on the topic of consumer finance and its consequences for the rest of us.

So without further ado . . .

This Week In Debt for 2/23/2025:

A new report from the Century Foundation and Protect Borrowers finds that one in four student loan borrowers is in default, and that things are going to get so much worse. (Write-up in WaPo here!) There is a ton to take from this report, but I’ll highlight two things:

Almost half of Black and Native borrowers and about one-in-three Hispanic borrowers are in default:

A second big wave of defaults is likely. Basically, 6.7 million borrowers have been in forbearance (that is, they haven’t had to make payments on their loans) because they were caught up in the litigation around the Biden administration’s efforts to make a new, more generous repayment plan called “SAVE.” The Trumps settled that suit by agreeing to kill SAVE, and so those 6.7 million people are about to enter repayment. And that’s likely to go badly. Per the report (emphasis added, citation omitted):

If the 6.7 million borrowers leaving the SAVE forbearance fall delinquent at the same 25 percent rate as the general population, 1.7 million more borrowers will fall delinquent. This brings the national total of borrowers in distress to nearly 17 million. But this figure is likely a floor, not a ceiling. The SAVE cohort is more financially fragile than the average borrower. When combining that vulnerability with the shock of suddenly higher payments, their delinquency rates will most likely exceed the national average.

Elsewhere in student debt:

Reuters: Navient borrowers begin receiving payments from consumer watchdog case

[The Private Student Loan Company] Ascent Closes $45MM Series C Financing Amid Growing Opportunity in the Student Lending Landscape (emphasis added):

Ascent, a leading provider of innovative financial products and student support services, today announced the successful close of its Series C funding round. Federal policy shifts that cap the amount of federal loans available for education are driving more students toward private lenders to help cover their tuition bills. The private student loan need is projected to double to $26B over the next three years, and Ascent is positioned to support these students looking to pursue their educational goals.

Talk about saying the quiet part out loud! Note also the discussion of “outcomes-based financing.”

I learned a new word, and it is “inquorate.” But actually: a cool op-ed argues that folks should challenge actions that agencies take when the Trumps have left those agencies lacking a proper quorum in their leadership ranks (emphasis added):

Thanks to term expirations, resignations, and presidential removal, agencies with significant vacancies include the Commodity Futures Trading Commission, which has one of five seats filled; the Federal Trade Commission, which has two of five filled; and the National Credit Union Administration, which has one of three filled.

Despite these vacancies, the agencies continue to act. Supporters argue that the absence of explicit, statutory quorum requirements allows any remaining officials to act—even when, in the case of the NCUA, the agency’s regulations provide that “agreement of at least two of the three Board members is required for any action by the Board.”

We question these assertions and encourage litigators already challenging these agencies’ actions to include quorum violations among their claims that the agencies acted unlawfully.

Get to work!

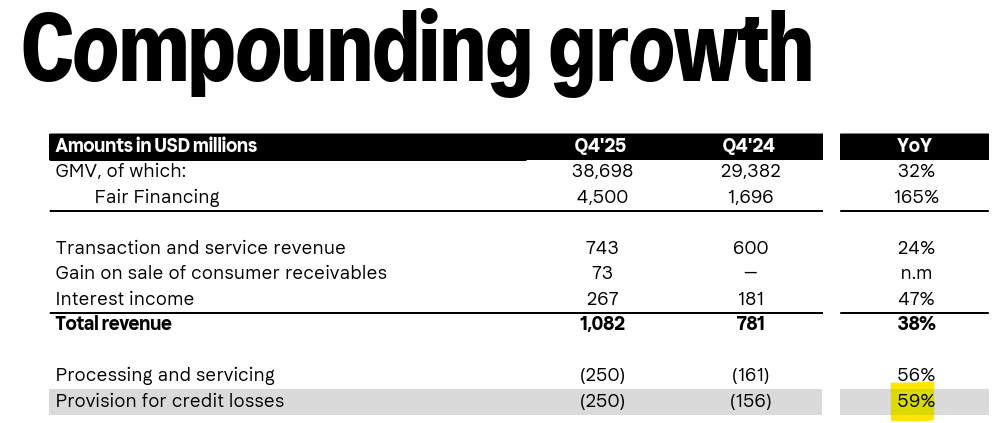

People have long wondered whether BNPL will ever be profitable, and the answer does not appear to be moving toward “yes” (emphasis added):

Shares in the payments firm are on course for their worst day since listing after Klarna reported a pretax loss of $241 million for last year, even as it pulled in record revenue.

What went wrong? The culprit seems to be that Klarna increased its provision for loan losses (that is, the amount it’s expecting to lose on bad loans) by 59 percent (highlight added, this image is from their earnings report):

This matters for consumers because unprofitable companies are more likely to make relatively unpredictable and risky moves to make a buck.

And while I know font week was last week, that header font from Klarna is just way too kooky.

Similar to our opening story: the Chairman of the CFTC just announced that he thinks that federal law preempts (i.e., blocks) any state-level efforts to regulate online gambling, because those online gambling markets are . . . somehow . . . actually not gambling markets?

From the Chair’s tweets:

Congress gave the @CFTC comprehensive authority over any contract based on a commodity, and the legal definition of a commodity is very broad.

And so only the CFTC can purportedly touch Kalshi when it offers a contract for “Men’s College Basketball Champion” or “Will the U.S. confirm that aliens exist before 2027?” (on the latter, the current number is 19.6 percent).

Reactions and relevant things:

Governor Cox@GovCoxMike, I appreciate you attempting this with a straight face, but I don’t remember the CFTC having authority over the “derivative market” of LeBron James rebounds. These prediction markets you are breathlessly defending are gambling—pure and simple. They are destroying the lives

Governor Cox@GovCoxMike, I appreciate you attempting this with a straight face, but I don’t remember the CFTC having authority over the “derivative market” of LeBron James rebounds. These prediction markets you are breathlessly defending are gambling—pure and simple. They are destroying the lives Mike Selig @ChairmanSeligI have some big news to announce…4:21 PM · Feb 17, 2026 · 992K Views201 Replies · 448 Reposts · 4.87K Likes

Mike Selig @ChairmanSeligI have some big news to announce…4:21 PM · Feb 17, 2026 · 992K Views201 Replies · 448 Reposts · 4.87K LikesKayla Scanlon tweets the following graph from Bberg:

Chair of the “Sports Betting Alliance” just outright tweets that his org got an online casino bill passed in Virginia by hiring the right lobbyist.

Elsewhere: “Starting today Substack authors can natively integrate data from the world’s largest prediction market [Polymarket].”

How’s private credit going?

The big private credit fund Blue Owl halted redemptions for its retail-focused product:

[I]nvestors in Blue Owl Capital Corp II, known as OBDC II, will no longer be able to redeem shares on a quarterly basis. Instead, the fund will return capital through periodic distributions funded by loan repayments, asset sales or other transactions.

The real heads know that the 2008 crisis officially began when the bank BNP Paribas halted redemptions in certain funds holding subprime mortgages. Hey, watch this space!

Sorry, this rocks. Former Goldman CEO Blankfein in WSJ discussing risks in private credit (emphasis added):

If something blows up and big institutional investors lose money, does the public sector care that much? Not really. If a bunch of individuals start losing their 401(k) plans and their money, does the public sector care? Does the government sector care? Yes, a lot.

I think it’s crazy to put those [private credit] assets there [in people’s 401(k)s] and I think it’s crazy from their [people in the private credit industry’s] point of view. They have nice lives, they make a fortune, their companies are huge, they already own their yachts and whatever it is they want. Why are you going into this dangerous territory just to make your business a little bit bigger when that represents such a big potential problem in the future? These securities are opaque and may be riskier than most, but to the extent you’re selling to institutions people don’t care that much. But if individuals lose money or insurance companies or real businesses lose money it’s terrible.

For those wondering how critically the OCC is going to supervise the Trump-linked “Erebor” Bank, to which the OCC just gave a bank charter: turns out the OCC also gave Erebor’s founder a novelty-sized physical copy of that bank charter.

More on Erebor here.

And finally, some potpourri:

WSJ: The Break Is Over. Companies Are Jacking Up Prices Again.

Job growth down >95% since 2021.

Goldman: the hit from rising electricity prices b/c of the data center buildout will fall hardest on lower income households.

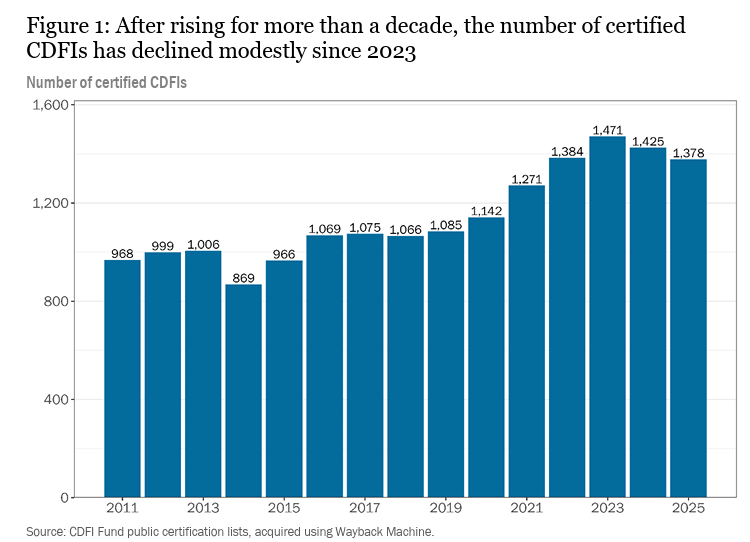

Things at Community Development Financial Institutions (i.e., institutions that help the underserved) are going badly:

Politico: Hassett says Fed staff should be ‘disciplined’ for reporting the US pays tariff costs (something something unitary executive theory)

Notre Dame College Republicans on the SCOTUS tariff case: “He who saves his country violates no law. We urge President Trump to defy the Supreme Court’s lawless, disgusting ruling today.”

“Humans today work fewer hours and have longer lives than any humans in history”

Style section:

The Traditional Architecture Likers in the White House are going to make the Ellipse asymmetrical to accommodate the new East Wing/ballroom.

As the Obama presidential library nears completion, gird yourself for many of the most inane, navel-gazing takes this side of Twitter.

JAGs sent to DOJ to help with habeas petitions related to DHS surge in MN are being held in contempt.

Rogan is maybe turning on Trump, take 89238945.

AI bot Claude identifies as Jewish.

NYT: Meta Begins $65 Million Election Push to Advance A.I. Agenda.

BLaw: Live Nation Loses Bid for Full Dismissal of Antitrust Suit.

“12% of Americans believe Noah of Noah’s Ark is married to Joan of Arc.” (h/t Claire Stein-Ross)

Good graph: contemporary oligarchs are historically stingy.

Fellow Substacker Curtis Sliwa: The Beats That Carried Me Through: Electronic Dance Music.

“Fascism didn’t just arrive in boots. It came in bouncy houses and Facebook mom groups.”

Rolling Stone: Is RFK Jr. a ‘Never Nude’?

Have a great week!

| A guest post by

|