This Week In Debt: 3/23/2026

Private credit student loan apocalypse? Also: zombie mortgages, credit cards, and more!

Hi,

The past week has thrown into stark relief how insane it was for the Trumps to make the student loan system reliant on private credit (emphasis added below):

A fund holding consumer and small-business loans made by companies including Affirm and Block is the latest corner of the private-credit market to come under stress.

Stone Ridge Asset Management told clients in the fund last week that recent redemption requests were so high that it would honor only 11% of the amount investors wanted back, according to an investor update viewed by The Wall Street Journal.

That suggests that investors’ concerns about private credit are broadening. Unlike other private-credit funds that experienced a flight of investors in recent weeks, Stone Ridge’s fund didn’t hold loans to software makers or other corporate sectors that investors fear will be displaced by advances in artificial intelligence.

Private credit, we say around here, is just a name for the part of the financial world where lenders make really big loans and then hold those loans on their balance sheets instead of selling, syndicating, or securitizing them. If that sounds dense, then here’s the point: the article above highlights how there is an ongoing pullback in private credit lending, and this Substack post posits that policy choices by the Trump 2.0 admin have made it so that problems in private credit are now likely to leave tons of people unable to afford an education.

I’ll explain. Recall that in passing the Big Bad Bill last year, the Trumps made the federal student loan system less generous so that private lenders could play a bigger role in education finance. That way, market-style discipline could maybe, just maybe (so the reasoning on the Right went), help reduce tuition rates at colleges. (Really, the change has probably just made it more likely that college will once again be unattainable for people who don’t already have means, but that’s for another Substack post.) Either way, the result so far has been that the private student lending business is booming.

To match the sudden surge in demand for student loans, private student loan companies have had to rely on private credit lenders as a source for the dollars that they (the student loan companies) will ultimately lend out to students. E.g., in an earnings call from January, the CEO of the student lender Sallie Mae said (emphasis added):

[W]e estimate that roughly 30% to 40% of our private student lending originations will flow through strategic partnerships [with private credit lenders], with additional balance sheet growth managed through seasoned portfolio loan sales.

For a sense of how many student loan dollars people suddenly need, here’s what Sallie’s CEO had to say about how much new lending his company expected to do post-Big Bill:

We believe that when fully phased in, PLUS reform could contribute an estimated $5 billion in annual originations for Sallie Mae representing approximately 70% originations growth over 2025.

And remember, meeting that demand requires (per the first quote) a huge slug of private credit dollars being available.

But now things in private credit are turning. Whereas in January I was reporting in these very pages that private credit was “diving headfirst into consumer debt,” the private credit sector has faced a wave of unexpectedly high defaults and attempts by investors to pull their money. (In a sign of the times, Bloomberg reported this past week that “JPMorgan, Goldman [are] Offer[ing] Hedge Funds [a] Way to Short Private Credit.”) You may have read about these issues more or less beginning in the software space, but pressures across the private credit landscape and beyond it are profoundly interconnected.

For private credit barons, that downturn may mean one fewer yacht. But for students, it could now mean no longer being able to go to college, as the lenders that students were relying on could soon find that private credit’s dollar spigot is closed. (And that’s to say nothing about how even lenders who don’t rely directly on private credit funding could end up being affected by larger fallout from a turn in that market.)

Perhaps the worst part is that we’ve seen this movie before. We used to have a system where most student loans were made by private companies and insured by the federal government, rather than the government just making the loans outright. But even those heavily-subsidized semi-private loans disappeared overnight when markets seized up during the Financial Crisis. The result was that the government had to bail out that semi-private student loan market to prevent a situation where millions of people wouldn’t have been able to afford an education because they happened to have enrolled during a crisis.

America eliminated that old program and moved to a system of direct government lending to students in part to make sure that whether people would be able to go to school wouldn’t centrally depend on whatever shifts and shocks happened to be going on in financial markets at a given time. But now millions of students who rely on loans to attend school could be in the lurch, all because Trump threw the student loan system to a pack of wolves that turned out to be over-exposed to software startups that ultimately had weak insulation from AI disruption.

Ok, ok, enough. Below, I have organized the best from the last week on the light, cheery topic of consumer credit. Let’s dive in.

So without further ado. . .

This Week In Debt for 3/23/2026:

They’re moving the student loans to Treasury. I mean, really, what is the point of this?

Right yes obviously the point is to make it so the Trumps can say they are closing/dismembering the Department of Education. They previously said they were going to move the student loan portfolio to the Small Business Administration, they moved some other educational programs to the Department of Labor, etc.

But like . . . if the things you do not like about the Department of Education are the things it does . . . and you are just moving those things to different places . . . oh my god slam my head against a wall.

Of course, it’s not that I think the Trumps should actually follow through on getting rid of these important government functions. It’s that the Trumps are undertaking symbolic moves that are likely to make service-deliver worse, all so that they can grab a headline. And that, I submit, is very dumb.

Bloomberg has a great write-up on “zombie mortgages.” These are generally second mortgages that people took on before the Financial Crisis but haven’t heard about in years, in part because many of the loans are now unenforceable under state statutes of limitation. Companies buy these forgotten loans on the cheap and do whatever they can to bully homeowners into paying (emphasis added below):

A Bloomberg News investigation last year found that more than 600,000 second mortgages taken out before the 2008 financial crisis — and then largely forgotten amid a wave of loan modifications during the recovery — remain outstanding across the country. Debt collectors buy these mortgages for pennies on the dollar and then demand homeowners pay bills that often include years of back interest.

If you can’t see it, the photo caption above says a company went after a 61-year-old immigrant in Maryland for $72,000 over one of these zombie loans. These loans are particularly nasty because debt collectors will threaten foreclosure (whether it’s actually available or not) unless homeowners cough up the giant sums they allegedly owe.

The article, though, is mostly about how the zombie mortgage industry appears to be going bare-knuckle in state capitals to resist accountability. E.g. (emphasis added):

In a room outside the Maryland State Senate chamber last winter, consumer advocates were meeting privately with lawmakers to explain how borrowers were losing their homes over “zombie” loans . . . . At the time, the legislature was considering a bill to protect homeowners from unfair attempts to collect these debts.

Then Robert Enten barged in. The lobbyist for the Maryland Bankers Association began shouting about his opposition to the bill, according to three people with knowledge of the event who asked not to be identified discussing a private conversation. Others began shouting back, and the meeting soon broke up. In the weeks after, the bill passed the House of Delegates unanimously but stalled in the Senate and died.

In addition to yelling, the industry recently sued to block consumer protections that were passed into law in California. Etc.

And of course, this is also yet another “the CFPB was doing something here until Trump 2.0 started” story (emphasis added):

The [CFPB] had been raising the alarm about zombie second mortgages since 2023 and was investigating at least three firms involved in collecting them, Bloomberg reported last year. A spokesperson for the CFPB said the enforcement effort has not been abandoned, but declined to elaborate.

Here’s a blog post on zombie mortgages that Lorelei Salas published when she was the CFPB’s Director of Supervision in the Biden era, perhaps as an opening salvo to presage further action. Oh, what should have been.

Elsewhere in bad mortgage/housing stuff:

The Urban Institute on “How Shared Equity Products Work, Who Is Using Them, and Regulatory Recommendations.” “Shared equity products” turn out to be equity-stripping loans that companies target toward people with (Urban’s words here) “low credit scores or income challenges.” For a sense of what goes on in this space, here is a lawsuit Massachusetts brough against the company Hometap for having “pervasively and systematically violated the state’s consumer protection laws, including mortgage and foreclosure prevention laws, putting financially vulnerable homeowners at high risk of losing their homes” (bold is mine).

Wired: Two Literal Crypto Bros Built a Real Estate Empire. Then the Homes Started to Fall Apart. (I’m including this because it involves “tokenized homes.”)

Bberg: Fannie, Freddie Place Large Bids for Mortgage-Backed Securities.

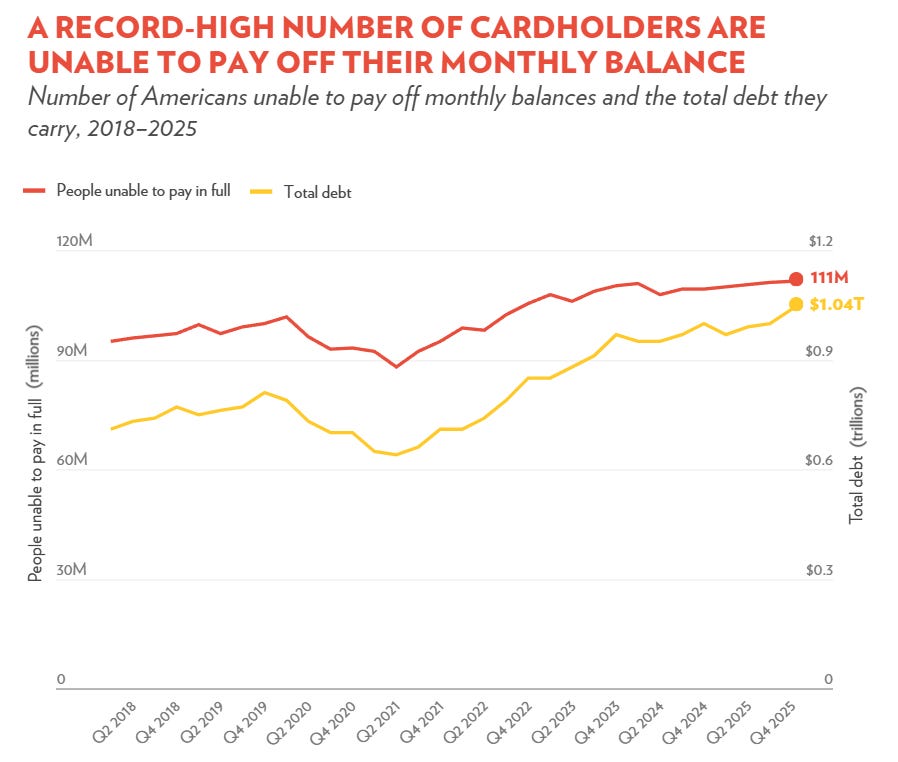

Horrifying new credit card data. Protect Borrowers and the Century Foundation published a report on how bad things are in the CC market, and they are quite bad (emphasis added below, also here’s a great thread from More Perfect Union summarizing the report):

[R]oughly half of active cardholders and 40 percent of U.S. adults are unable to pay their credit card bills in full and carry a balance from month to month. This translates to roughly 111 million people trapped in cycles of persistent debt and exposed to industry-inflated, record-high interest rates. Of that group, more than 27 million Americans can only afford the minimum payment each month.

The report additionally finds that Americans have paid a record-setting amount of interest as a result of credit card banks doubling their profit margins over the last two decades. Americans have paid a cumulative total of $2.1 trillion in credit card interest since 2010, which is more than the total amount of outstanding student debt, and the total amount of auto loan debt, owed at the end of 2025. Since President Trump took office, Americans have paid $134.5 billion more than they would have under a 10 percent interest rate cap.

Elsewhere in credit cards:

Interesting LinkedIn post from Ben Brown on how a lot of the CC industry is now sort of just a competition for affluent users’ annual fees.

Carter Dougherty in Open Banker, on swipe fees and the Credit Card Competition Act: Banks Don’t Wanna Compete.

The Trumps push for the banking system to be $200 billion less stable. Last week, Trump’s people at the Fed proposed reducing Financial Crisis-era capital rules in such a way as to remove $200 billion of cushioning from the banking system. (Here’s my explainer on what bank capital is and how it works.) The upshot is that this will make the banking system more fragile just as its $300 billion of exposure to private credit comes under the microscope. (And that’s just an area of risk we know about!)

The proposals introduced by the Federal Reserve and other regulators would hand a major victory to big banks, which had resisted sharply higher requirements proposed under the Biden administration. Wall Street’s embrace of a second Trump administration had largely centered on the prospect that plans for those stricter requirements would be scrapped.

The last time the Trumps pushed bank deregulation, the crises at Silicon Valley Bank, First Republic, and Signature followed close behind. As they say: first as tragedy, then as farce.

Also: a good, more weedsy thread on these changes from BankRegBlog.

Elsewhere: there is apparently a deal on the “stablecoin market structure bill,” but we don’t have details yet. Those details appear, however, to involve a trade where community banks get a little sprinkle of their own deregulation. It’s a fitting ending: the saga of the stablecoin market structure bill has highlighted the tensions that sometimes arise for the Trumps when they try to offer goodies separately to crypto and banks, so it makes sense that the solution would be just to offer goodies to everyone.

And finally, some potpourri:

Arizona files criminal charges against Kalshi, alleging it allows illegal gambling (I bet they did that because Kalshi very obviously allows illegal gambling.)

I wrote the other week about the Mr. Beast’s kid-focused finance app (kiddie Earned Wage Advance!). Now, Genna Contino at MarketWatch has a great read on the notorious Evolve Bank, which is behind the app:

A very cool new paper from Roosevelt’s Brad Lipton in the Harvard Law Journal on Legislation website: “Statutory Hammers: Legislative Drafting in an Age of Cynical Litigation.” From the abstract:

Over the past decade, cynical litigation in our federal courts has fundamentally altered the operation of the administrative state. Agency rulemaking now unfolds against a backdrop of forum shopping and activist judging that often derails regulation from ever taking effect. This Article argues that Congress should respond to this dynamic by deploying strong statutory default provisions—“hammers”—that take effect absent timely agency action. . . . A comparative case study of mortgage lending and debit-card interchange-fee regulation under the Dodd-Frank Act illustrates how legislative design can determine whether Congress’s intent gets reflected in policy or instead is an empty gesture.

A sign of what’s to come: an AI “compliance” startup appears to have been a total fraud, potentially putting people at risk of criminal liability.

Meta is killing off the metaverse. It lost $80 billion on it.

Bookmark it: Palantir is launching an AI-based mortgage platform.

Fascinating thread about the wild services ultra high net worth people get from private bankers:

Private school, private colleges, internships, jobs, the right fraternity, the right spring break, safety while traveling abroad, leniency from childhood misdemeanors, etc. these are the differentiating services.

The Style Section:

Crystal Bridges, perhaps a perfect midcentury modern.

Frank Lloyd Wright’s architectural details.

‘The guy’s a piece of s--t’: SBF’s pardon push falls flat in Congress.

NY Mag: How [yet] another gutsy Forbes 30 Under 30 start-up founder got in trouble with the Feds.

Former CIA acting director John McLaughlin is available for hire as a DC-area party magician.

Peter Thiel continues giving talks saying that everyone he doesn’t like is the antichrist. (Spiritually related throwback: once, while on acid, John Lennon called a meeting of the Beatles to tell them that he had realized he was the reincarnation of Jesus.)

Rapper Afroman wins lawsuit against police over mocking their 2022 raid in viral music videos.

Have a great week!

| A guest post by

|