This Week In Debt: 3/9/2026

Bilt's train wreck is a CFPB story, EWA, auto, and more.

Hi,

For a sense of how damaging the Trumps’ dismantling of the Consumer Financial Protection Bureau (CFPB) has been for consumers, look no further than the slow-moving train wreck at the credit card company Bilt.

To review (and, to be clear, Jason Mikula at Fintech Business Weekly has the definitive write-up of the underlying facts here): Bilt is a startup that offers a credit card that has the special perk of being usable for rent payment. While most people either can’t charge their rent on a credit card or have to pay a convenience fee to do that, Bilt users can charge their rent without a fee and while earning credit card reward points. Neat!

Bilt got Wells Fargo to be the bank underlying that credit card by promising that Bilt users would eventually start using it paying for other stuff beyond rent, and that those people would eventually start carrying balances on their cards. Wells would probably lose money on the rent rewards, but the bank would make up for that when users started paying for other stuff (that is, through interchange revenue) and carrying balances (that is, by generating interest revenue). And through cross-selling opportunities, etc.

But, oops! Those promises never came to fruition, and by 2024 Wells Fargo was losing “$10 million every month” on its partnership with Bilt. Per reporting in the Journal, it turned out that the young, high-income people who were likely to get Bilt were the same kinds of people who are likely to be strategic around credit card use. The result was that Bilt users would just pay their rent on the card, pocket their rewards points, pay off their card balance when it came due, and not use the card for anything else. That meant Bilt didn’t get the additional interchange or interest revenue it had promised Wells.

I mean, it may not stun you to hear that I initially found this story kind of funny. Bilt’s young CEO Ankur Jain (who is himself the son of a tech guy whose Wikipedia page includes a “Crash and fallout” subsection, and not one talking about a car crash!) charmed Wells Fargo into handing a bunch of money to high-income yuppies at Wells’s expense. Ankur, you scamp!

But then Wells killed the partnership, and Bilt had to scramble to rejigger its business model. That’s where things got hairy. Needing to turn the ship around, Bilt released a new slate of cards in January called “Bilt 2.0.” Those cards would be powered by Column Bank, which does a lot of fintech stuff. For our purposes, it suffices to say that The 2.0 cards are less generous than the 1.0’s. Existing Bilt users could keep their account with Wells and get a Wells credit card, or they could move to Bilt 2.0 with Column. If they chose the latter option, Bilt promised the transition would be “seamless.”

But oops, that transition appears to be going horribly. Per Jason M’s article mentioned above, social media is now being “flooded” with complaints including (bold added):

Users who claim outstanding balances were transferred from Wells Fargo to the new cards without their permission;

Users who complain they’ve experienced difficulties making payments on outstanding balances still held at Wells Fargo;

Users who claim they received a new Wells Fargo Autograph card they didn’t want or authorize;

. . .

and, perhaps the issue that has driven the most frustration and outrage, issues with rent and mortgage payments not being made, being delayed, or bouncing, with some users reporting their external bank account had been debited by Bilt, but the corresponding payment was never made to their landlord or mortgage servicer.

And folks who have tried to get support appear to be getting routed to a crappy AI chatbot. E.g., to that last bullet (highlight is mine):

That’s where the Bilt saga becomes an illustration of how bad Trump and his allies’ dismantling of the CFPB is for actual people. In normal times, and under existing law, these consumers would/should be able to submit complaints to and expect a substantive response from the CFPB to address Bilt and Wells’s errors. In addition, the CFPB could right now be using its wide range of tools to ensure that Bilt and Wells get their collective act together, and that consumers emerge from this episode unscathed. Instead, the Trump-selected leadership at the Bureau has continued to “slash” the agency’s supervisory function and walk away from enforcing the law, all while trying to gut consumers’ ability even to submit complaints to the Bureau.

As Jason’s article mentions, this isn’t just a matter of bad customer service. Instead, Bilt may be violating consumer protection laws like the CARD Act and improperly pooling users’ rent payments in a single bank account. But with the CFPB on the sidelines, even clear violations of federal consumer protection law would lack their key enforcer.

That’s what it really means for Trump and allies including Elon to have dismantled the CFPB. Bilt’s CEO fumbled his business model and its revamp, but he’ll be fine—in fact, his wife is rumored to be joining the next season of the Real Housewives of New York. Wells, meanwhile, just got a sweetheart deal from the CFPB to get out of a consent order related to the bank’s notorious 2018 fake accounts scandal.

Real people, on the other hand, could right now be having their rent or mortgage payments get bungled by a fintech company, and America’s central consumer financial protection agency isn’t allowed to do so much as bat an eye. States need to fill the breach, sure—but none of this is okay.

Alright, alright, I’ll calm down. Below, I have hunted and gathered for you all the best of the last week on the topic of debt. Savor it.

So without further ado (and with a new background color!). . .

This Week In Debt for 3/9/2026:

Earned Wage Advance (EWA) lenders are losing their battle against reality. A common theme around here and at Protect Borrowers generally is that consumer finance companies often try to say that their loans are magically not loans for legal purposes—even, of course, when they obviously are—and that you should kindly take your consumer financial protections elsewhere. Among those companies are EWA lenders, which in THIS house we refer to as payday lenders with better websites. (More detail on EWA here.)

EWA companies and their friends disagree, insisting instead that EWA loans are not loans. But they are wrong. Last week, in a case about whether the fintech “Klover” violated the Truth in Lending Act (TILA) and the Military Lending Act (MLA) when it made loans at interest rates that exceeded “1200%,” a federal judge said the following (h/t Jonathan Joshua, emphasis added):

Every federal district court to have confronted arguments similar to those Klover makes here has rejected them and held that the TILA and MLA apply to Earned Wage Access products and that tips and expedite fees like Klover’s constitute finance charges, notwithstanding defendants’ attempts to characterize their EWA products as non‑recourse.

. . .

Rather than recapitulate these sometimes lengthy analyses, this court adopts their reasoning and rejects the arguments Klover advances in its motion to dismiss. In so doing, this court adds its voice to the growing chorus of decisions that have concluded that similar cash advance programs constitute “credit” within the meaning of the TILA and that tips and expedite fees, on facts similar to those alleged in the instant complaint, are plausibly alleged to constitute finance charges.

Ha, nice.

In Bankrate, new reporting on how things are very bad in subprime auto lending:

The article is basically an overview of the space. As an illustrative example of how things work in subprime auto lending, the article recounts the story of one Terry Holmesly, a real person who bought a Chevy Equinox and financed it through their auto dealer’s credit partner (emphasis added):

Despite making on-time payments, Holmesly is now “upside down” on the Equinox. Her lender made that a foregone conclusion by:

Setting the sticker price ($21,695) as much as $7,000 more than online asking for this model with about as many miles (76,080) at the time

Wrapping $4,465 worth of optional “add-ons” she didn’t fully comprehend, including nonessential gap coverage and a warranty into her loan balance

Allowing her to finalize the transaction with a 3.6% down payment (far lower than experts typical recommendation of 10 to 20%)

Bringing into question whether the terms meet the National Association of Consumer Advocates’ (NACA) standard of predatory lending: using “deceptive or unethical means to convince you to accept a loan under unfair terms”

The article goes on to describe how inadequate existing protections are around auto financing, how some states police this area “more aggressively than others,” and how consumers have vanishingly few tools to protect themselves here.

Banks v. crypto. One thing I talk about a lot here is that the Trumps’ efforts to give handouts to both the crypto and banking industries sometimes inflame tensions between the two. This week, the inflammation continued (emphasis added):

Kraken’s banking unit has won access to the Federal Reserve’s core payment systems, making it the first crypto firm to be able to move money on the same rails used by thousands of banks and credit unions.

The approval of the so-called master account at the Fed will allow the unit, Kraken Financial, to handle transactions more quickly and seamlessly for big clients and professional traders, the company said.

The bank lobby is mad about this because the payments system has historically been their thing. (More info.) And so, see, e.g., the Bank Policy Institute (emphasis added):

We are deeply concerned that the Federal Reserve Bank of Kansas City has approved an account request for a “limited purpose” master account—which appears to be a “skinny” account—before the Federal Reserve Board has finalized its policy framework for those accounts. This action ignores public comment that the Federal Reserve sought on this framework, and it was issued with no transparency into the process for approval or the risk mitigants that have been imposed to address the very significant risks it raises.

And the Independent Community Bankers of America (emphasis added):

ICBA and the nation’s community banks are very concerned with the Federal Reserve Bank of Kansas City’s approval of a master account for Kraken Financial. Granting nonbank entities and crypto institutions access to the master accounts traditionally limited to highly regulated insured depository institutions poses risks to the banking system.

Lots of concern! Meanwhile, adding insult to injury, Trump appears to be siding with crypto world in the big ongoing “banks v. crypto” fight related to the so-called “crypto market structure” bill. (More on that fight here.)

Elsewhere: Crypto Firm Zerohash Applies for National Trust Bank Charter.

They’re going after liquidity rules. Debt Serious has a great write-up for the third anniversary of the fall of Silicon Valley Bank (SVB), arguing in part that we’ve overlooked the role SVB’s relatively poor liquidity position had in precipitating the bank’s demise. “Liquidity” generally refers to how much of a bank or company’s assets are in things that can move quickly, like cash, and liquidity is important to maintain because it helps institutions respond to unexpected demands for outflows.

The issue is that more liquid stuff usually earns less yield, so there’s an incentive for each individual bank to be less liquid than might be optimal for the system as a whole (that is, because they’d rather hold higher-yielding assets, even if they’re less liquid). To resolve that issue, regulators basically just tell financial institutions they have to maintain some minimum level of liquidity whether they like it or not.

But the “or not” folks are in charge now, and they’re doing their thing (emphasis added):

Saying that bank liquidity is “the next big-ticket item” for regulatory reform, top officials at the Treasury Department and Federal Reserve today outlined their case for revisiting the liquidity coverage ratio to recognize discount window borrowing capacity.

In prepared remarks for a Washington, D.C. roundtable on bank liquidity, Treasury Secretary Scott Bessent said the current framework for regulating liquidity, created in response to the 2008 financial crisis, “has excessively and unnecessarily limited banks’ ability to do what they are supposed to do — lend.”

The Fed is on board too:

“After years of recognized flaws, we have yet to address these known weaknesses,” [Fed Vice Chair for Supervision Michelle] Bowman said. “The consequences are clear. Banks create additional buffers by hoarding high-quality liquid assets rather than lending. This liquidity hoarding reduces credit availability to the economy. In addition, by increasing the demand for reserves, it also requires the Fed to maintain a larger balance sheet to meet that demand.

Sure, that’s bad. But at the very least, the Debt Serious example shows we could one day get some good Substack posts about whatever comes next.

The good folks at the California Policy Lab updated their consumer credit tracker with new data. They report the updated figures paint “a split financial picture across the state. Mortgage lending is rebounding — driven by large home loans in the Bay Area — even as many other borrowers fall behind on student loans and mortgages.”

Click through for a cool dashboard you can play with.

How’s private equity doing? (h/t Ben Carlson)

Elsewhere (in private credit): BlackRock Slashed Private Loan Value From 100 to Zero [just three months after valuing at 100], US private credit defaults hit record 9.2% in 2025, Fitch says.

And finally, some potpourri:

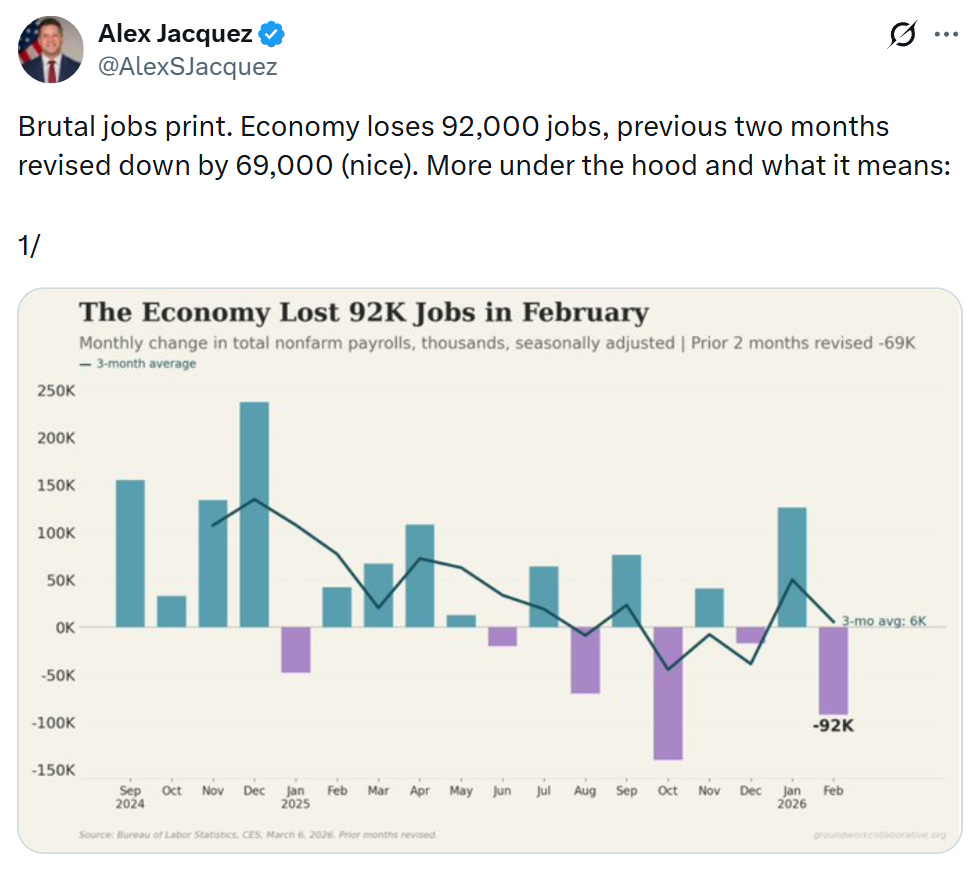

Groundwork’s Alex Jacquez offers a deep dive into last week’s terrible jobs report:

The Economic Populist: Trump Says He Wants Wall Street Out of Housing. Elizabeth Warren’s Got a Plan.

WSJ: Ted Cruz asks Treasury to approve $200 billion [capital gains] tax cut without Congress. CBPP on what that would look like:

The Economist: America’s welfare state is more European than you think [because “State-level policies are making up for stingy federal provision”]

The CFTC updated its logo, and eh. Seems pretty uninspired. And apparently they just updated the CFTC logo in Trump 1.0?

New paper from the Fed on the history of monetary independence.

Trump drops name-and-shame lawsuit against law firms, then picks it up again.

100 years later, it’s time for the U.S. to reconsider zoning.

The Style Section:

Application to buy a medieval castle in Transylvania asks for blood type.

Have a great week!

| A guest post by

|