OpenAI Now Does Consumer Finance. What Could Go Wrong?

This Week in Debt: May 18, 2026

Hi there,

Today, Mike writes in for our opening with a quick take on OpenAI’s blockbuster announcement last week of a partnership with Plaid.

On Friday, OpenAI announced a deal with ChatGPT and Plaid, the fintech company that facilitates a range of private companies’ access to your banking information. Tech evangelists heralded this announcement as a new milestone in the breakneck evolution of Artificial Intelligence (AI)—the first time one of the AI giants moved directly into finance, rather than licensing its LLM to fintech firms to engage in various kinds of financial schemes.

It’s easy to see how quickly this type of deal will evolve into AI agents making financial decisions on behalf of their users—not just recommending investment and budgeting strategies, but promoting specific financial products and services. That outcome may feel like the future, but it is really the past. A private company building a tool that advises users on financial decisions is a tale as old as the internet. Mint.com walked so ChatGPT could run (promotions for high yield savings accounts or meme coins).

Consumer financial law is ready for this moment. Despite what you may read about the need for bespoke regulation to rein in the risks posed by AI, here in America’s deeply financialized economy, Congress actually saw around this corner. The Dodd-Frank Wall Street Reform and Consumer Protection Act, passed in 2010 in the aftermath of the financial crisis created the Consumer Financial Protection Bureau (CFPB) with a set of flexible tools and legal authority to police nonbank financial firms across the economy—including firms providing financial advice, brokering financial products, and providing services to financial companies. CFPB also has the authority to supervise, on an emergency basis, any nonbank provider of a consumer financial product or service that poses risks to consumers. It can demand data and it can send subpoenas. It should do all of these things and more.

We’ve written a lot about the state of Trump’s CFPB. So have others. The watchdog is now a shadow of its former self, with priorities that feel more like the hybrid of a bank lobbyist’s wish list and a right-wing think tanker’s fever dream than anything resembling a robust consumer protection agenda.

Fortunately for readers of IN DEBT—including those of you advising your financial services clients on compliance matters—what CFPB can do today matters less than what the law requires of companies and what may follow in the weeks, months, or years to come. That’s particularly true because financial regulators in California and New York have complementing authorities to the embattled federal consumer watchdog and do not need to wait for the political tides to turn in Washington to start asking questions and taking actions to protect working families.

If I were the Commissioner of the California Department of Financial Protection and Innovation or the Superintendent of the New York Department of Financial Services, I’d have a framework ready to go to monitor the conduct of the LLMs themselves—particularly now that these models are sucking information about users’ finances directly out of the banking system and telling us how to manage our money.

There are obvious, unanswered questions here as OpenAI pushes forward into personal finance. From data security to conflicts of interest and kickbacks, regulators have an obligation to surface risks and protect borrowers.

We don’t need to look very far to see how conflicts of interest can snowball quickly. A team of AI researchers published a paper a few weeks ago that found that *every single AI model,* when pressed to advise a user about the cheapest options for air travel, promoted sponsored options that were more expensive. What happens when this is a mortgage, a credit card, or a student loan?

The early evidence suggests that Big Tech is very sensitive to the emerging consensus that it’s using your personal information to lie, cheat, and steal from you. Groundwork Collaborative’s Lindsay Owens made headlines earlier this year for a viral tweet that laid out the case against Google’s Gemini for what appeared to be a complex agentic surveillance pricing and upselling scheme. The company was indignant but not quite Shermaneque in its denials. If your PR strategy hinges on convincing customers that “[t]he term “upselling” is not about overcharging,” you’ve probably lost the messaging war.

Does an AI agent that can operate autonomously and use what appears to be its own judgment to advise you on how to manage your money constitute a risk to consumers? Clearly.

Do you have any way to protect your own interests when an AI agent tells you it’s giving you the best advice for you, but it’s really the best advice for its secret business partners? The answer is clearly no, and the conduct itself appears to violate a wide range of federal and state laws.

While the Trump Administration looks the other way, state financial regulators and law enforcement can and must stand in the gap.

And now, folks, it’s time for the best from the past week in consumer finance. So without further ado. . .

This Week In Debt for May 18, 2026:

And now back to Ben.

Arbitration agreements. I graduate from law school at the end of this month, which is to say that I can still remember a time when I was not entirely lawyer-brained (though: I am still not a lawyer and nothing I say is legal advice!). One thing I remember from that pre-law school era is the intuition that while we all sign a bunch of contracts throughout our day (online terms and conditions, check-boxes where you agree to certain corporate policies, etc), those contracts probably contain some horrifying set of magic words that will absolutely blow up in your face if the company on the other end wants them to.

Law school did not exactly uh disabuse me of that intuition, and now, from the National Consumer Law Center (“NCLC,” emphasis added below):

Today, 25 consumer advocacy and other public interest organizations condemned Bank of America’s decision to insert a forced arbitration clause in the fine print of its Online Banking Service Agreement. Forced arbitration blocks customers’ access to the court system and eliminates their right to a jury trial when they are harmed, instead forcing them into biased, closed-door proceedings where consumers rarely win. It also prevents people from joining together in class action lawsuits to fight back against systemic harms.

Right, BofA is going to insert a magic incantation into its online banking contract that will make it so that you basically can’t sue them for any reason if you are one of their customers. They actually can do that! Instead, if BofA hurts you and you try to sue them, they now get to shuffle you into a backroom where you, an individual person, will have to negotiate . . . with the second largest bank in the United States. Meanwhile, the supposedly neutral third party overseeing this negotiation (that is, the arbitrator) will be a repeat customer of the bank, meaning they will be someone hugely incentivized to go easy on BofA. I mean, you can see why banks like this.

NCLC recounts the history of BofA’s arbitration term, which is revealing (emphasis added):

In 2009, Bank of America, along with Capital One, JPMorgan Chase, Discover, and HSBC were defendants in an antitrust lawsuit in which credit card borrowers alleged that these banks, and other large banks, colluded to implement arbitration provisions in their credit card agreements to prevent their customers from enforcing their rights under state and federal law in individual and class action cases. As a result, Bank of America stopped using its consumer contracts to force customers into binding arbitration. And for almost 17 years, Bank of America customers retained the ability to hold the bank accountable in the public court system.

But the new forced arbitration clause also prohibits customers from joining their claims together in class actions to seek justice when systemic, widespread harm occurs. This is particularly harmful to consumers with small-dollar claims, which they couldn’t afford to pursue on their own.

That is, they stopped having an arb agreement for a while as a concession, and now they’re back to using one. An indication that they know this is bad behavior!!!!

People can opt out of the new arbitration provision, but the clock is already ticking (people have 60 days from the “first delivery of the arbitration provision,” which already happened). And, you know, most people don’t read this newsletter.

All to say: I recently wrote about how people should just be able to void predatory terms in take-it-or-leave it consumer contracts, and there are a number of countries where people basically can do that when it comes to arbitration agreements. In fact, the set of countries where people can generally void arbitration agreements used to include the United States but industry pushed a number of bad-faith and pretty obviously dubious legal arguments throughout the 20th century to make it impossible for Americans to get out of arbitration terms, and industry largely succeeded. That path took us to the situation where we find ourselves now, which is, I submit, pretty insane (see the description above beginning “they now get to shuffle you into a backroom . . . .”).

The NCLC press release highlights legislation some folks have introduced in Congress to fix all of this, and I just think that fighting against arbitration should be much more at the center of any consumer agenda for a next pro-consumer presidential administration. Project 2029 etc? Let’s get to work.

Elsewhere: Here’s a cool new book on the history of arbitration in the US by Brendan Ballou, who recently wrote that book “Plunder” about private equity companies.

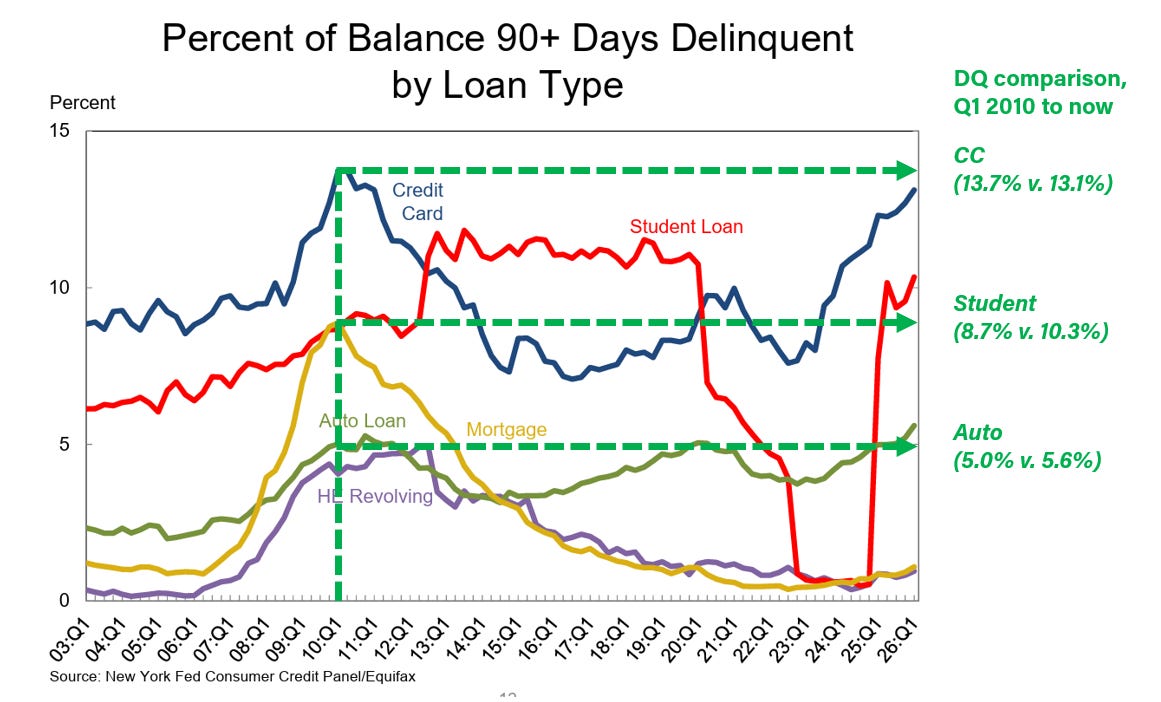

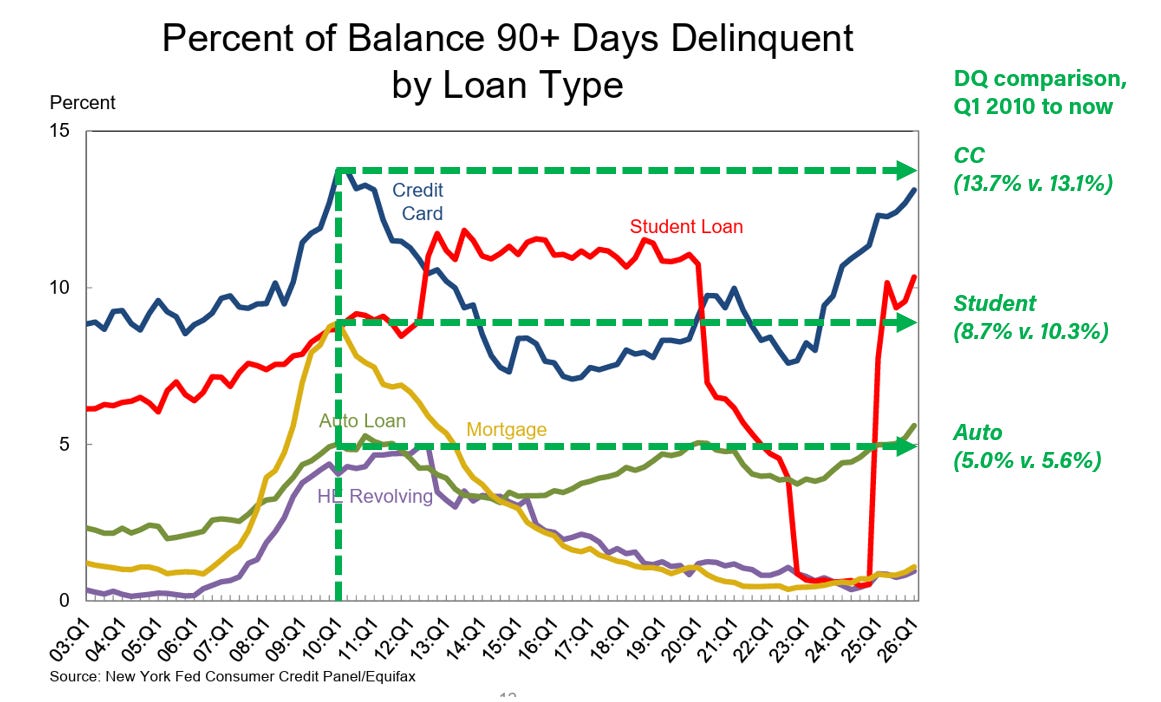

We’re facing record delinquencies on consumer debt. You almost certainly saw this already if you read this newsletter, and PB did a statement on it, but anyway: the New York Fed published some new data on consumer debt, and those data show we’re at the highest delinquencies ever for auto loans (or I mean the highest in FRBNY’s consumer credit panel), the highest delinquencies since the Financial Crisis for credit cards, and the highest delinquencies since COVID for student loans. Here’s an update to my famous Green Lines Graph, noting the comparison is to Q1 2010 just because that’s sort of the peak for Crisis-era delinquency in the FRBNY data:

I’m not a betting man, but it does seem like just a matter of time before CC and student also break their all-time records, no?

Elsewhere at the New York Fed: Federal Student Loan Defaults Return After Pandemic Pause. A team at the bank finds that defaulters on federal loans are getting older, are NOT just people who were already struggling before COVID, and are more likely to be past due on other kinds of debt (emphasis added):

[T]he share of student loan balances past due [has] increased, nearing pre-pandemic levels at just over 10 percent. . . . We find that the average borrower entering default is nearly 40 years old, was not past due on their student loans prior to the pandemic, and is more likely to live in the South. While defaulted borrowers are more likely to be past due on other forms of debt, the overall scope of student loan defaults is still relatively low, suggesting that fears of broader contagion to other credit products are premature.

New reasons to be worried about private student loans. We’ve talked about how Trump’s changes to the federal student loan program are meant to push more students toward private student loans, ostensibly to impose market discipline on tuition and students’ curricular choices. My main complaints so far have been that, in reality, those changes are mostly likely to produce some combination of a) people taking on increasingly hideous private loans for the same education, and b) academically qualified students just not going to school anymore because they can’t afford it.

But at Business Insider, Ayelet Sheffey introduces us to reason c) to be worried about the oncoming rise of private student lending: the private student loan market is just kind of a mess (emphasis added):

A construction manager in Massachusetts thought her $55,000 student-loan debt was forgiven — until she was sued. A Michigan nurse wanted to make payments on her balance of more than $50,000, but no one could tell her who to pay.

Their experiences point to a growing concern: As more Americans turn to private student loans, critics say the industry operates with uneven oversight, limited transparency, and fewer borrower protections than the federal student-loan system.

Not a great place for us to be dumping millions of new borrowers, particularly with the lights out at the CFPB and state AGs already stretched thin. To the point, Ayelet digs into how things in the private student loan space were going even before the changes in the Big Bill (emphasis added):

Private lenders serve about 10% of borrowers, yet account for roughly 25% of CFPB complaints. In reviewing the past 10 years of complaints, Business Insider found hundreds of entries related to lender mistakes with loan transfers, missing or erroneous documentation, and confusion about payment status. CFPB released a report in January showing it received about 4,500 private student-loan complaints from July 2024 through July 2025 — an increase of 33% compared to the previous year.

Seems bad! Stay tuned.

Banks and bank regulators behaving badly.

Erebor. A thing in American life now is that there are a bunch of actions where if you or I took them, we would go to jail, but if an AI chatbot or someone connected to the Trump admin does them, nothing happens. Erebor is a new Trump and Thiel-connected bank that just got a national charter (in record time!), and just like that: Erebor is pitching banking services to “top Venezuelan officials,” who are generally otherwise sanctioned.

Here’s some info on the penalties mere mortals like us would face for violating sanctions.

The OCC approved . . . what? The Office of the Comptroller of the Currency is the government agency that approves national bank charters. They have uh really been going hog-wild on that as of late, which is to say that during the Trump 2.0 admin they have been racing to approve stuff like Erebor (above), crypto schemes, crypto schemes that get hacked soon after getting a charter, etc. This week, the OCC gave conditional charter approval to something called “Augustus,” which appears to be an AI-something something bank focused on improving payment clearing. Their founder is 25, but rest assured, he has connections to Peter Thiel, so it’s ok. (BankRegBlog is skeptical.)

Elsewhere in “What the hell is the OCC doing?,” this time with the Fed’s help: the conversion of United Texas Bank.

Preemption. We’ve recently been talking about preemption, which for our purposes is where the OCC says that states actually cannot protect their consumers, and that only the OCC can make rules around banking. OCC affirmed its commitment to preemption this week, issuing “two final rules” saying basically that states can’t make banks pay interest on certain funds that those banks are holding in escrow.

Don’t you feel much better now?

On the bright side: California’s Department of Financial Protection and Innovation “Secures $1 Million Settlement with Yotta Technologies for Deceptive Practices.” We can call this story sort of bank-adjacent.

Elsewhere: FDIC released a report on the spring 2023 bank failures (SVB, Signature, etc) picking apart what made folks more/less likely to run.

Also: here’s a story about an FDIC employee repossessing a jet plane in 1976.

Ugh fine, crypto. Senate Banking passed the CLARITY Act (that is, the big crypto “market structure” bill), which now goes to a vote in the broader Senate. Gaudeamus igitur.

Humor me. I don’t really like writing about crypto, mostly because it all still seems to be just a solution in search of a problem? Like I obviously concede that everyone in crypto is still getting hilariously wealthy except for me/you, that crypto has become a massive lobbying force, that number go up, etc. But like, none of this appears to actually be delivering meaningful products/services for people even like 2 decades into the “crypto revolution,” voters don’t really seem to care about it, and even when governments have taken steps to facilitate crypto things, there is still a certain . . .

That is, as I once said: “even if public digital money is substantively a good idea, I don’t see how it gets over the Social Network problem: government money just isn’t cool.” I was talking there about certain ideas related to central bank digital currencies, but the same logic applies to idk “government approved crypto” like what the CLARITY Act delivers.

Anyway, the real story for me (as we talked about last week) is how the fight around the crypto bill pits two of the most whiny and entitled lobbies in DC against each other, and how the results amount to tremendous content. That story did not let up as the committee markup proceeded!

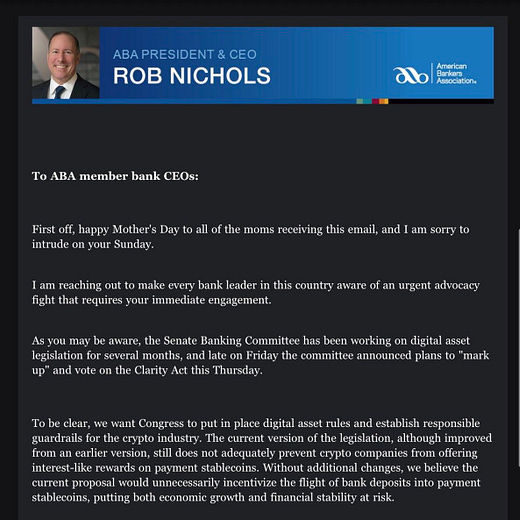

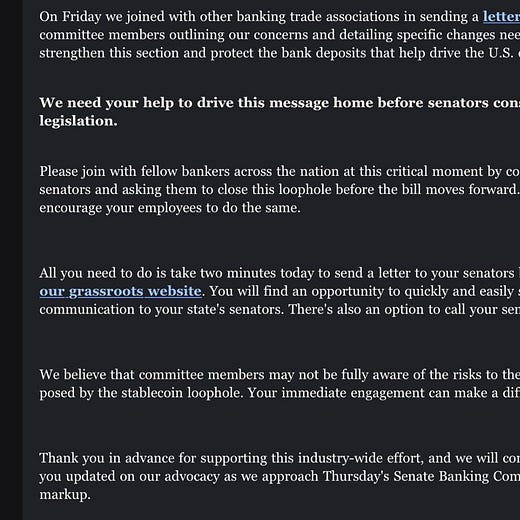

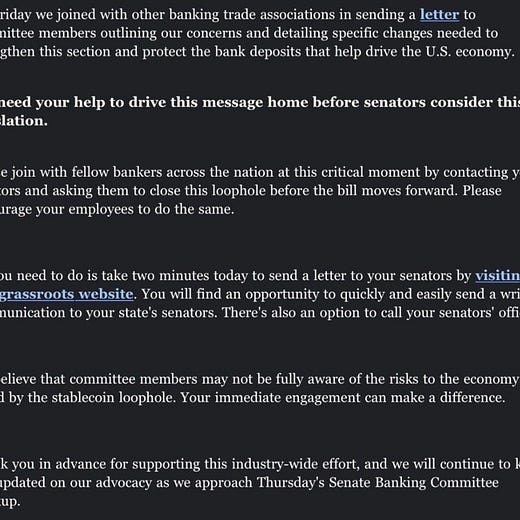

First, the American Bankers Association put out a statement encouraging member banks to contact lawmakers about concerns with the bill:

Brendan Pedersen@BrendanPedersenAmerican Bankers Association CEO Rob Nichols sent the following letter on Sunday to every other bank CEO in the country, asking bankers for “immediate engagement” on stablecoin yield policy. Senate Banking Committee is slated to mark up landmark crypto bill Thursday

Brendan Pedersen@BrendanPedersenAmerican Bankers Association CEO Rob Nichols sent the following letter on Sunday to every other bank CEO in the country, asking bankers for “immediate engagement” on stablecoin yield policy. Senate Banking Committee is slated to mark up landmark crypto bill Thursday

1:24 PM · May 11, 2026 · 438K Views83 Replies · 85 Reposts · 406 Likes

1:24 PM · May 11, 2026 · 438K Views83 Replies · 85 Reposts · 406 LikesThen everyone freaked out. Here’s Patrick Witt, the White House person in charge of advancing the crypto bill, responding to the ABA statement:

Patrick Witt@patrickjwittI specifically requested the attendance of Mr. Nichols and other bank trade CEOs at the meetings we hosted back in February to resolve the stablecoin rewards/yield issue. They refused. I guess the White House was beneath them? In their defense, I wouldn’t want to have to defend

Patrick Witt@patrickjwittI specifically requested the attendance of Mr. Nichols and other bank trade CEOs at the meetings we hosted back in February to resolve the stablecoin rewards/yield issue. They refused. I guess the White House was beneath them? In their defense, I wouldn’t want to have to defend Brendan Pedersen @BrendanPedersenAmerican Bankers Association CEO Rob Nichols sent the following letter on Sunday to every other bank CEO in the country, asking bankers for “immediate engagement” on stablecoin yield policy. Senate Banking Committee is slated to mark up landmark crypto bill Thursday2:45 PM · May 11, 2026 · 359K Views236 Replies · 721 Reposts · 3.45K Likes

Brendan Pedersen @BrendanPedersenAmerican Bankers Association CEO Rob Nichols sent the following letter on Sunday to every other bank CEO in the country, asking bankers for “immediate engagement” on stablecoin yield policy. Senate Banking Committee is slated to mark up landmark crypto bill Thursday2:45 PM · May 11, 2026 · 359K Views236 Replies · 721 Reposts · 3.45K LikesAnd Ohio senator Bernie Moreno:

Bernie Moreno@berniemoreno🚨 The banking cartel is in full panic mode. 🚨 While Americans were celebrating Mother’s Day with their families, the CEO of the American Bankers Association sent a frantic alert to every bank CEO in the country, demanding “immediate engagement” to lobby Senators and kill

Bernie Moreno@berniemoreno🚨 The banking cartel is in full panic mode. 🚨 While Americans were celebrating Mother’s Day with their families, the CEO of the American Bankers Association sent a frantic alert to every bank CEO in the country, demanding “immediate engagement” to lobby Senators and kill

2:18 PM · May 11, 2026 · 921K Views457 Replies · 2.48K Reposts · 8.58K Likes

2:18 PM · May 11, 2026 · 921K Views457 Replies · 2.48K Reposts · 8.58K LikesAnd the guy in charge of the “Digital Chamber” [of Commerce? of Secrets?]

Cody Carbone@CodyCarboneDCThe arrogance is astounding. For months, the banking lobby refused to engage on stablecoin rewards. They didn’t make this a red line during the GENIUS Act. They didn’t stop the House from advancing CLARITY. Now, days before markup, after months of saying “we won’t negotiate,”Brendan Pedersen @BrendanPedersenAmerican Bankers Association CEO Rob Nichols sent the following letter on Sunday to every other bank CEO in the country, asking bankers for “immediate engagement” on stablecoin yield policy. Senate Banking Committee is slated to mark up landmark crypto bill Thursday2:02 PM · May 11, 2026 · 50.1K Views34 Replies · 144 Reposts · 761 Likes

Cody Carbone@CodyCarboneDCThe arrogance is astounding. For months, the banking lobby refused to engage on stablecoin rewards. They didn’t make this a red line during the GENIUS Act. They didn’t stop the House from advancing CLARITY. Now, days before markup, after months of saying “we won’t negotiate,”Brendan Pedersen @BrendanPedersenAmerican Bankers Association CEO Rob Nichols sent the following letter on Sunday to every other bank CEO in the country, asking bankers for “immediate engagement” on stablecoin yield policy. Senate Banking Committee is slated to mark up landmark crypto bill Thursday2:02 PM · May 11, 2026 · 50.1K Views34 Replies · 144 Reposts · 761 LikesAnd the general counsel of Coinbase:

Paul Grewal@iampaulgrewalMaybe the CEO didn't get the message from the people actually in the room at the WH in meeting after meeting. We've already had "immediate engagement." You got "idle yield" killed. I know because I was there--you weren't. Take yes for answer. Move on. Stop wasting the time of

Paul Grewal@iampaulgrewalMaybe the CEO didn't get the message from the people actually in the room at the WH in meeting after meeting. We've already had "immediate engagement." You got "idle yield" killed. I know because I was there--you weren't. Take yes for answer. Move on. Stop wasting the time of Bernie Moreno @berniemoreno🚨 The banking cartel is in full panic mode. 🚨 While Americans were celebrating Mother’s Day with their families, the CEO of the American Bankers Association sent a frantic alert to every bank CEO in the country, demanding “immediate engagement” to lobby Senators and kill2:50 PM · May 11, 2026 · 230K Views106 Replies · 360 Reposts · 2.54K Likes

Bernie Moreno @berniemoreno🚨 The banking cartel is in full panic mode. 🚨 While Americans were celebrating Mother’s Day with their families, the CEO of the American Bankers Association sent a frantic alert to every bank CEO in the country, demanding “immediate engagement” to lobby Senators and kill2:50 PM · May 11, 2026 · 230K Views106 Replies · 360 Reposts · 2.54K LikesAnd then here’s two more fun ones from Patrick Witt, unrelated to the ABA thing:

Patrick Witt@patrickjwittI’m so impressed that Elizabeth Warren stayed up all night to read the 300+ pages of the CLARITY Act and deliver an objective assessment of the bill’s merits and not just some knee-jerk reaction. This is what true public service looks like. John Bresnahan @bresreports.@SenWarren, top Democrat on the Senate Banking Cmte, opposes the GOP crypto market structure bill released late last night12:53 PM · May 12, 2026 · 228K Views368 Replies · 328 Reposts · 2.41K LikesPatrick Witt@patrickjwittThe deals will continue until CLARITY improves.Brendan Pedersen @BrendanPedersenNews in PBN texts: Judiciary Committee Chair Chuck Grassley and Sen. Cynthia Lummis have a deal to address law enforcement concerns in a landmark crypto bill, per two sources familiar. The deal allows prosecutors to bring AML charges against demonstrably culpable crypto actors4:55 PM · May 11, 2026 · 38.7K Views18 Replies · 100 Reposts · 772 Likes

John Bresnahan @bresreports.@SenWarren, top Democrat on the Senate Banking Cmte, opposes the GOP crypto market structure bill released late last night12:53 PM · May 12, 2026 · 228K Views368 Replies · 328 Reposts · 2.41K LikesPatrick Witt@patrickjwittThe deals will continue until CLARITY improves.Brendan Pedersen @BrendanPedersenNews in PBN texts: Judiciary Committee Chair Chuck Grassley and Sen. Cynthia Lummis have a deal to address law enforcement concerns in a landmark crypto bill, per two sources familiar. The deal allows prosecutors to bring AML charges against demonstrably culpable crypto actors4:55 PM · May 11, 2026 · 38.7K Views18 Replies · 100 Reposts · 772 LikesMy god! The tone of these people! “I guess the White House was beneath them”! “The banking cartel”! “The arrogance is astounding”! And so on!

There are actually real substantive concerns here (e.g., anti-money laundering compliance), and it is striking that community banks were basically totally boxed out from the final negotiations around the CLARITY Act. The banks seem to be viewing this as halftime, though, so rest assured that they will still be going to bat on implementation/rule-writing stuff—and that there will be much more content to wring out of this fight.

And finally, some potpourri:

Former CFPB Director Rohit Chopra tapped to lead California’s new cabinet-level consumer agency. (The right people are unhappy about this.)

Capital One announces free coffee every Monday at Capital One Cafés this summer.

Antitrust:

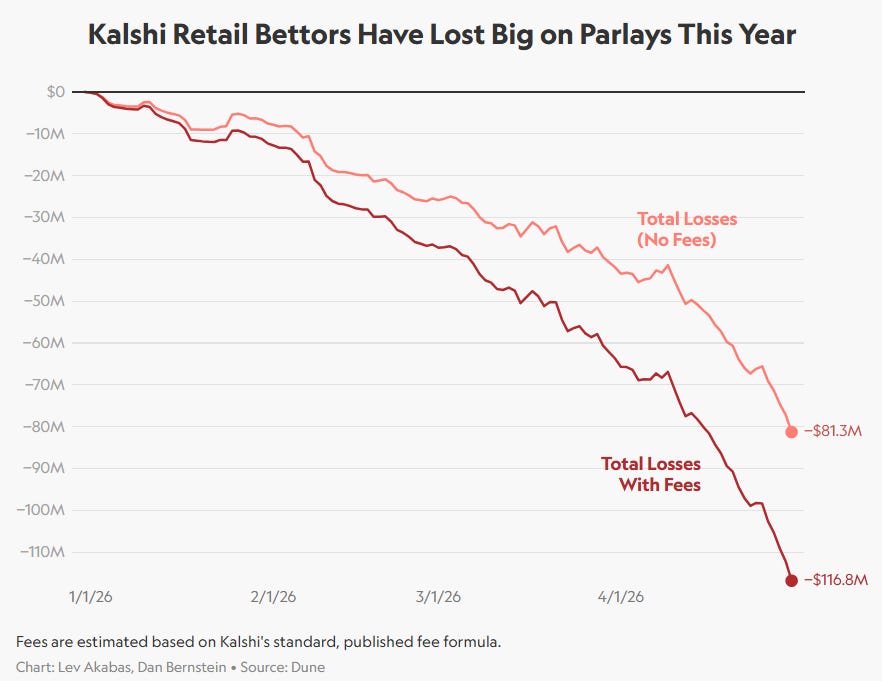

Dan Bernstein and Lev Akabas at Sportico: Kalshi Retail Bettors Have Lost $100M+ on Parlays This Year. (Really more than $110 million?)

Elsewhere: CFTC says certain “event contract transactions” (i.e., gambling) don’t have to be reported to swap data repositories.

The Style Section:

The CFTC updated its seal. Old seal here. I mean, the old one was bad, but what a missed opportunity. (Elsewhere, not quite recent but the new CIA logo and brand identity deserve some mention.)

The Poolio of Don Julio.

“By day, I’m one of the most feared asbestos litigators in the country. By night, I am Felix Darkmantle, the most notorious assassin in the Kingdom of Kurm.”

Apparently Ben Shapiro’s media empire is falling apart, and, perhaps more interestingly, there is drama (plagiarism accusations!) about the reporting of that story.

Meet Joseph Palmer, who was “persecuted” for being the first American to have a beard.

NYT: Archaeologists Find Egyptian Mummy Buried With the ‘Iliad’. (This is an excuse for me to share one of my favorite videos ever.)

After 30 years in prison and 3 “last” meals, Richard Glossip is out on bail. (Recommended reading). And apparently Kim Kardashian paid his bail.

{kind=link}

{kind=link}

Have a great week!

| A guest post by

|