This Week In Debt: 2/2/2026

A requiem for the Kardashian Kard, and so much more.

Hi,

There was a lot of news last week at the intersection of celebrity and money (Jennifer Garner’s company IPOing! An assertion that I could not otherwise substantiate that Tiger Woods had something to do with last week’s failure of Metropolitan Capital Bank & Trust, the first bank failure of the year!).

So, noting Kanye’s recent apology for . . . everything . . . lets dial it back to 2010 and talk about the saga of the Kardashian Kard. (I am, as always, indebted to Bonnie Latreille for this one.)

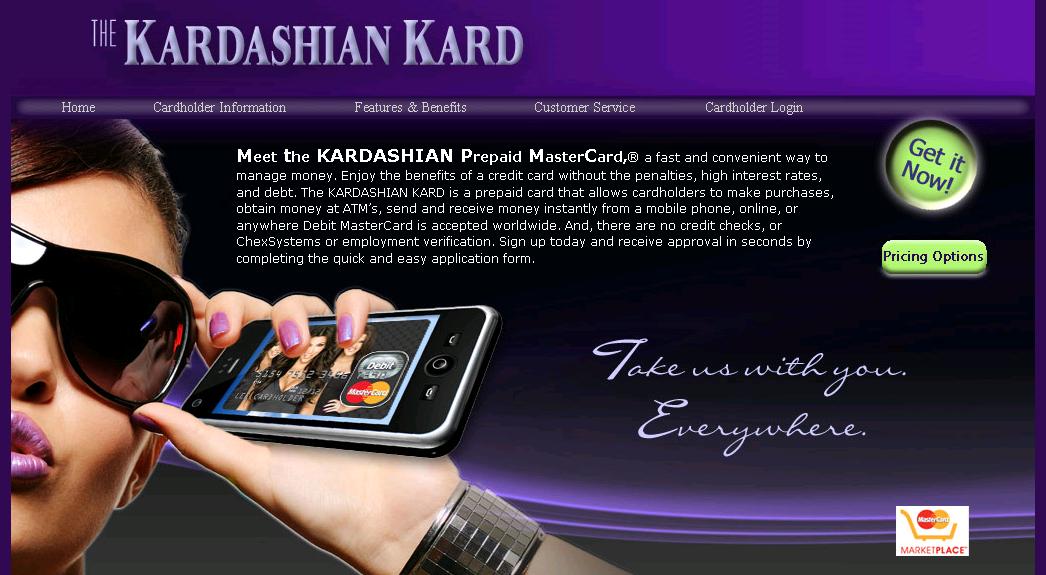

On November 9, 2010, as Keeping Up With the Kardashians ruled the airwaves, Kim, Khloé, Kourtney & Co launched a prepaid debit card in partnership with MasterCard and University National Bank. “Now our fans will be able to take us with them everywhere,” the sisters apparently said in a press release that I cannot find.

Just about immediately, the entire world noticed that the card was a) “being promoted to teenagers—who, presumably, are gullible enough to want to keep up with reality show stars,” and b) just absolutely loaded with fees. Brad Tuttle reported at the time that those fees included:

$59.95 in fees just to use the card for six months

$99.95 (alternately) in fees to use the card for one year

$7.95 monthly fee after that initial phase ends

$9.95 card replacement fee

$1.50 ATM withdrawal (domestic, in addition to whatever fee is charged by the ATM bank)

$1 ATM fee if your card is declined

$1 fee if you try to spend money with the card and it’s declined

$1.50 fee to talking to a live service center operator

$6 fee for canceling your account and getting your money refunded by mail

Not good! To be fair, style is priceless.

Unfortunately, criticism of the kard quickly began piling up. Consumer Reports, for example, said the kard “Comes Loaded With Hidden Fees & Weak Protections,” though they conceded that those are the same problems present in “Other Prepaid Debit Cards.”

Then the law got involved, with then-Connecticut Attorney General (and now Senator) Richard Blumenthal threatening an investigation and writing the K’s a letter saying, “I am deeply disturbed by this card’s high fees combined with its appeal to financially unsophisticated young adults. In reality, no family can ‘keep up with the Kardashians’ using this card’ . . . .” Lol.

(Blumenthal really did make a meal out of all of this, though rest assured he had actually already been elected to the Senate by the time the kard stuff blew up. E.g., an article at the time cites Blumenthal saying the following in addition to the letter mentioned above [emphasis added]:

“We’re warning parents that these so-called Kardashian Kards are really an outrageously expensive form of pre-paid debit card that belies the promise of affordability,” Blumenthal said, adding the cards “also send the wrong lessons about managing money.”

“These debit cards should be destined to failure, but they seem to exploit the Kardashian image or aura of luxury and extravagance,” Blumenthal said.

Criticism not just of the kard, but of the Kards! A bit ad hominem [ad feminas?], methinks.)

Per the K-clan’s lawyer, Blumenthal’s letter was the last straw:

“The Kardashians have worked extremely long and hard to create a positive public persona that appeals to everyone, particularly young adults,” wrote the [family’s] lawyer, Dennis Roach.

“Unfortunately, the negative spotlight turned on the Kardashians as a result of the Attorney General’s comments and actions threatens everything for which they have worked.”

By November 30, 2010 (recall: that’s three weeks after the launch), the Kardashian Kard was kaput. University National Bank halted sales, Blumenthal was “pleased,” and the K’s pulled out of a deal that let the bank use their names and likenesses. Only 250 people actually got one of the kards, and I can’t tell if that number is high or low.

The Kardashians eventually got sued for $75 million over their pulling out of the name/likeness deal, but a judge tossed that case. Consumers also got “refunds of balances and up-front fees.”

We can laugh now, I guess, because the damage appears not to have ultimately been that great. (Though there is a website called “thekardashiankardruinedmylife.com” that you can read). The Kardashians went on to face criticism (including, notably, from pre-breakdown Kanye) regarding the extent of in-app fees associated with the “Kim Kardashian: Hollywood” game, to settle with New Jersey for “charging consumers in New Jersey sales tax on items that are exempt under state law” through Kim’s Skims clothing brand, etc.

(I also found this extremely chatty and honestly pretty bitchy blog post from a press person in the office of Washington’s Attorney General, which described the Kardashians as “attractive, if slightly vacant, media darlings,” and said, “I’m guessing that the Kardashians, known for their plasticity, didn’t immediately grasp the irony of being depicted on pieces of plastic.” Man, the things people used to say in 2010!)

There is maybe a more substantive consumer finance angle here (Blumenthal noted at one point that the cards were “not linked to a bank account, so they’re not subject to any government regulation or oversight”), but eh. Let’s just pour one out for 2010, funny consumer finance floatsam, and the things we may not have expected to carry on from the past.

Now, let’s get to the best of the last week in consumer finance. See below for links, musings, and more!

So without further ado . . .

This Week In Debt: 2/2/2025

Let’s start with our beloved Consumer Financial Protection Bureau:

Weaponized telework: Some stories about financial regulation are actually about telework. As the initial COVID shock dragged on, the Biden admin tried to make certain telework opportunities for federal employees permanent. The Trumps, however, disliked telework, in part because COVID was “fake” to begin with, and in part because Trump himself is skeptical of what teleworkers do all day (“They’re going to be going out. They’re going to play tennis. They’re going to play golf.”). So Trump took a bunch of steps to limit telework by federal employees after he re-took office.

Then last week, this happened (emphasis added):

Consumer Financial Protection Bureau examiners sidelined by the Trump administration will be back on the job as early as April, but the number of exams they conduct and the scope of their supervision will be cut back dramatically [from ~600 exams per year to ~70].

. . .

And all exams will be conducted virtually, rather than having examination teams travel to review company records and speak with employees in person, the people said. That’s a stark change from previous agency practice.

I mean, this is ideologically consistent to the extent that the Trumps appear to believe that work done remotely is necessarily subpar. You could imagine a very funny scene where Trump hands CFPB acting director Vought a file called “top secret devious plan to make federal agencies ineffective,” and Vought shudders and asks “boss, are you sure?” as he opens to a piece of paper that just says “telework.”

For more serious commentary, CFPB alumnus and current Roosevelt Institute-r Brad Lipton explained on Twitter that supervision is “one of the gov’ts most powerful law enforcement tools to catch big financial institutions stealing from people,” and that the broader kneecapping of the Bureau’s supervisory function is an example of how the Trump 2.0 admin has “turned its back on working people.” (Because yes what’s at issue here isn’t just the tele-aspect of the changes the Trumps are making; the Trumps are also substantively narrowing the underlying exams.)

Restored Bureau funding comes with a touch of grey: There was recently a big fight about whether the Bureau’s funding was legal. One consequence of that fight was that it created the risk that the agency would be so hobbled (that is, defunded) as to be unable to keep the deregulation train rolling. As I said at the time regarding some of the Bureau’s efforts to worsen certain consumer protection rules, “Can’t do that if the lights are off!”

Welp, it turns out that the opposite is true too. The funding thing has been resolved—CFPB acting director Russ Vought lost in court about it, and he then graciously caved into compliance. But now that the lights are back on, it does seem the Trumps are getting back to their dastardly, well-lit work:

The Consumer Financial Protection Bureau, fresh off a $145 million cash boost, plans to move back to a traditional process for rewriting a Biden-era open banking rule, leaving the fintech data access policy in a prolonged limbo.

The CFPB will undertake a formal notice-and-comment rulemaking process after initially stating it would issue an interim final rule to implement closely watched changes to the 2024 regulation . . . .

They had previously been planning to do a quick and dirty “interim final rule,” and now they’re doing a real one.

I’m being a little cute above, because the open banking thing isn’t actually just a straightforward regulatory rollback. It’s really a fight that pits banks against fintechs/crypto companies regarding who gets access to your financial data, and at what cost. In the rule above, the Bureau will essentially have to mediate between two key pro-Trump donors/constituencies (i.e., banks and fintech/crypto). More detail here. It’s sure to be interesting . . . and litigious!

But either way, as much as a funded Bureau is a better Bureau, in the meantime there will be trade-offs to our having one.

Elsewhere: Consumer guardrail facing cuts waits on court decision.

The Trumps are going after consumer complaints: One of the most important things the Bureau does is take in and address complaints from consumers. Those complaints are public, and you can peruse them here.

Complaints historically both led directly to consumer relief (because the Bureau would intervene on people’s behalf when companies weren’t responsive) and helped the Bureau identify areas of harm/set priorities. The complaints were good and important.

So naturally, the Trumps appear to be going after the Bureau’s compalint function:

The CFPB is publishing this notice and soliciting comments on: (a) Whether the collection of information is necessary for the proper performance of the functions of the CFPB, including whether the information will have practical utility; (b) The accuracy of the CFPB’s estimate of the burden of the collection of information, including the validity of the methods and the assumptions used; (c) Ways to enhance the quality, utility, and clarity of the information to be collected; and (d) Ways to minimize the burden of the collection of information on respondents, including through the use of automated collection techniques or other forms of information technology.

That is, the Trumps are asking some pointed questions about the Bureau’s complaint collection. Can’t be good! Recall that the question of whether the Bureau’s complaint portal would remain intact briefly became a flashpoint during Trump 1.0.

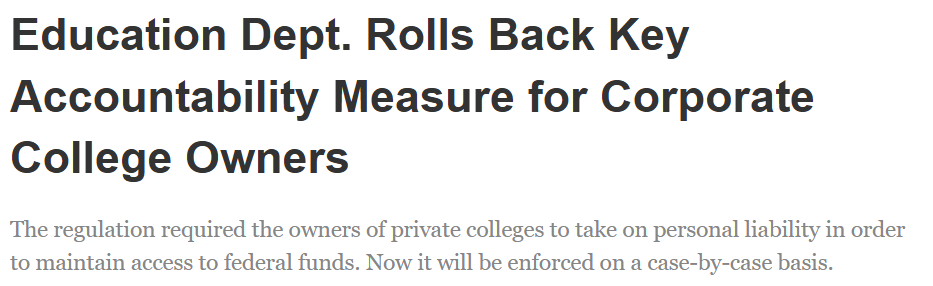

For-profit college deregulation: On the one hand, the Right talks a big game about hating government waste/fraud/abuse. On the other hand, the Right has a pretty dedicated aesthetic commitment to supporting stuff that appears to be market-flavored. These things can sometimes come into conflict, such as when it turns out that a hugely outsized portion of the fraud/abuse/harm in higher ed turns out to be at for-profit colleges.

Hmmm, guess alongside me how the Trumps chose to resolve this tension last week (emphasis added below):

The Trump administration will no longer automatically enforce an accountability measure for the owners of private institutions that consumer advocacy groups say is critical to protecting students and taxpayers.

. . .

Under the policy, primary owners of for-profit and nonprofit colleges were required to sign onto a contract, known as a Program Participation Agreement, in order for their institution to access federal student aid. The aim of requiring the individual or corporation who owns an institution to sign onto the PPA signature requirement was to hold them accountable for unpaid debts, misuse of federal funding and compliance with federal aid law. (PPAs still have be signed by the president or CEO of the institution.)

Unstoppable force meets extremely movable object.

Elsewhere in for-profit college land: Student Loans May Get Discharged And Refunded Automatically For 200,000 People As Key Deadline Passes. This is about the Sweet case, which is about borrowers who were defrauded by bad for-profit schools:

Many borrowers already have received student loan forgiveness under the Sweet v. Cardona (now Sweet v. McMahon, renamed after the current Secretary of Education, Linda McMahon) settlement agreement. But a separate group of borrowers was supposed to have their Borrower Defense applications decided earlier this week. If that didn’t happen [and for many, it didn’t], under the terms of the settlement agreement, these borrowers would be entitled to full relief including automatic discharges and refunds of past payments they made on the covered student loans.

The era of consumer protection in New York City under Department of Consumer and Worker Protection Commissioner Sam Levine just keeps getting better (emphasis added):

Late last week, [New York City’s Department of Consumer and Worker Protectio} sued Radiant Solar and its owner, William James Bushell, demanding $18 million in restitution and about $1.7 million in penalties — the largest sum the city has ever sought from a home improvement contractor.

The city contends that Radiant Solar engaged in a dizzying array of mechanical and monetary malfeasance for years. According to the lawsuit, filed with the city’s Office of Administrative Trials and Hearings, Radiant’s solar panel systems often failed to deliver the energy savings it had advertised and sometimes did not work at all.

The company padded loans with hefty and undisclosed kickbacks to lenders, failed to see projects through to approval by the city and did not file paperwork for customers to receive tax credits, the suit says. It also ran a bogus sweepstakes for a new Tesla, according to the suit.

A “dizzying array of mechanical and monetary malfeasance”! And of course, where there’s fraud, a Tesla is never far away.

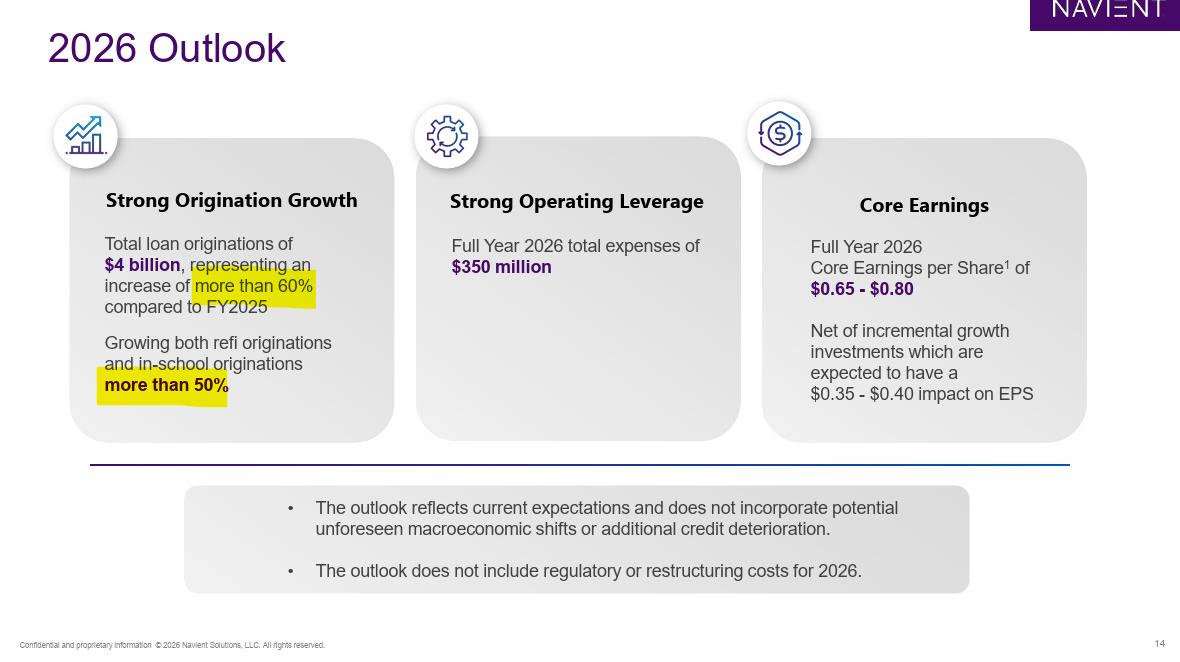

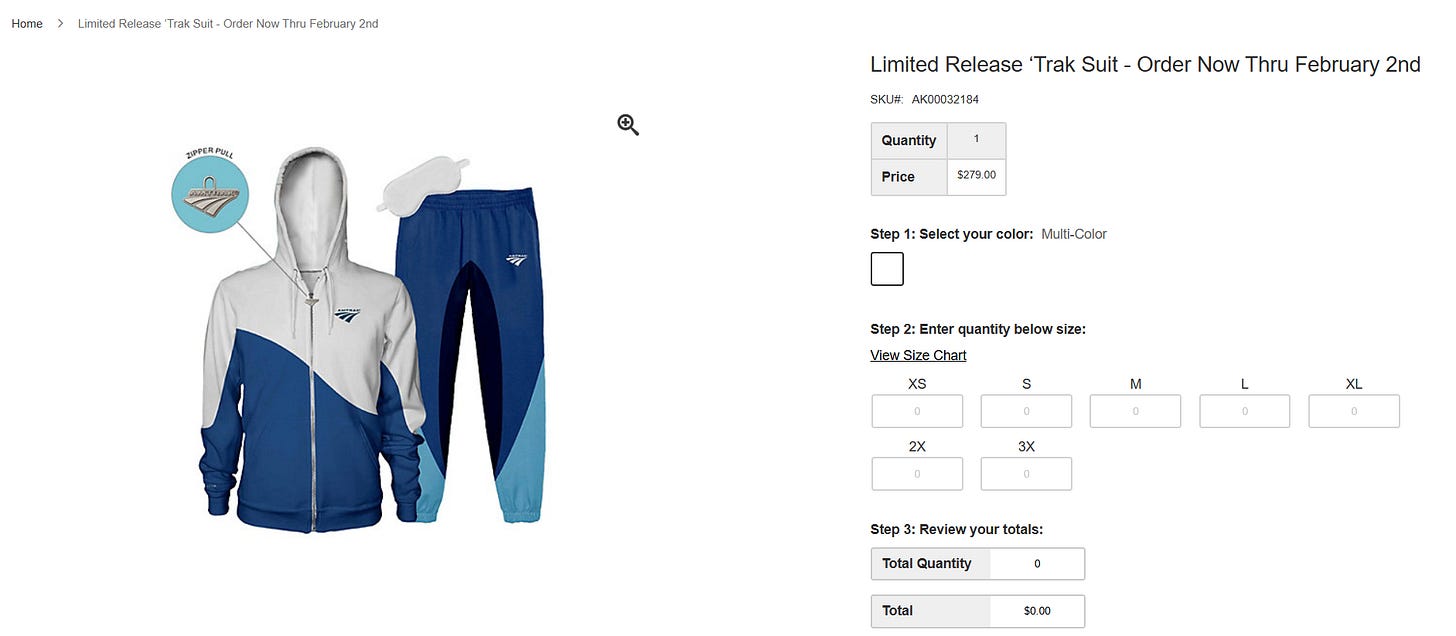

The student loan company Navient announced its earnings last week, and their results sort of tell the story of the specific way in which things are currently bad for consumers in the student loan market. On the one hand, from their earnings presentation (highlights mine):

On the other hand (highlights still mine):

Recall: Navient is a company that does a bit of private lending to students alongside a bit of student loan refinancing, and that also has a big pile of old loans that are insured by the federal government. (Recall further that the student loan system used to be based on private companies making government-insured loans; that was the FFELP program, and those are the “FFELP” loans above.)

Navient’s earnings show that business is booming in private lending as people continue refinancing (because rates went down) and needing additional private in-school credit (because the Big Bad Bill restricted the availability of federal loans). But at the same time, people who already have loans are struggling the pay them back.

That’s in part because the two groups at issue here are slightly different. Those remaining federal borrowers are people who have been struggling for a while (after all, FFELP loans were discontinued way back in 2010). In contrast, the new borrowers are, by definition, people who are already creditworthy enough to get private loans.

The point is that the picture here is consistent with where we’re headed in student lending generally, and how the Trump admin’s policies are going to leave people behind on higher ed access. You’re either already creditworthy, and you can get private loans and attend school, or you’re not, and you will be left to struggle.

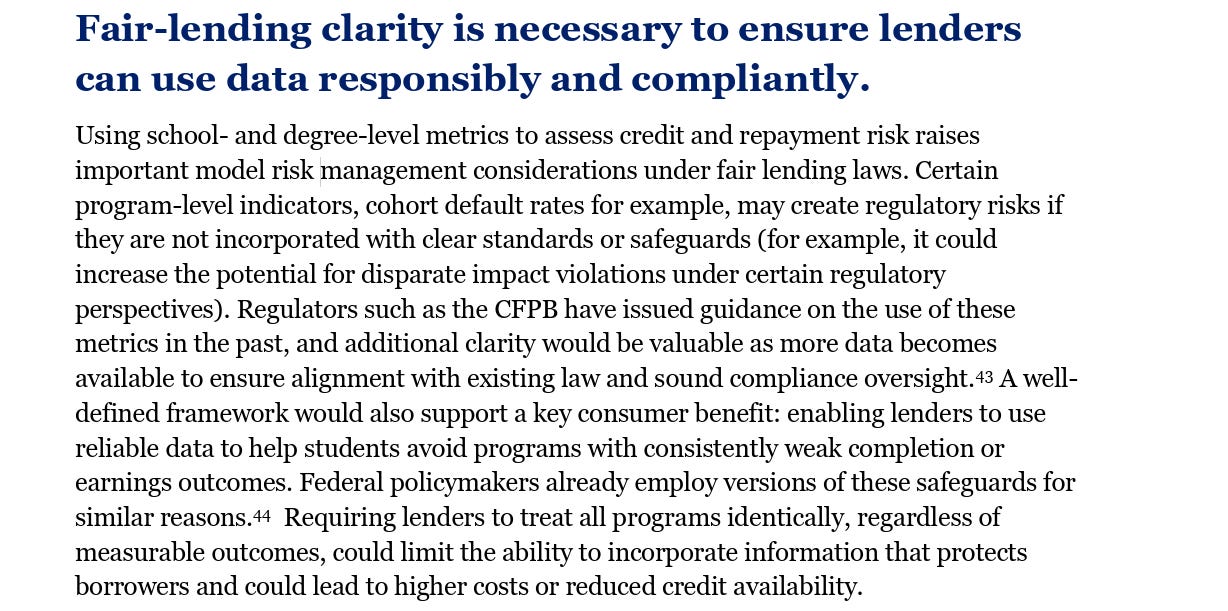

Meanwhile, this is . . . a fascinating document from the Consumer Bankers Association (CBA):

Basically, CBA observes that like one-in-four students probably won’t be able to get the private loans necessary to attend college given the changes in the Big Bad Bill, and then proposes some very

lucrativenice changes it would like so that it can make sure nobody has to forgo education.Big takeaway: CBA appears to really want its member lenders to be able to discriminate. Specifically: a big aspect of fair lending law is that you have to decide whether or not to lend to someone and at what rate based on individualized factors like someone’s credit score (yes there are problems with credit scores), and not based on group identity. So you can’t, for example, make lending decisions based on cohort default rates. Student loan companies have gotten in trouble for doing that.

But CBA wants the rules to change (really, they are doing the thing where industry pretends there is not regulatory clarity because the regulation is not what they would like, then asks for preferred changes under the guise of calling for “clarity.”):

Pretty strange to call for “clarity” while noting that the CFPB has already issued guidance on this in the past. When Protect Borrowers was SBPC, we caught a student loan company more or less pricing loans based on cohort-level student outcomes, and look at that—in a world with labor market discrimination, using those metrics just meant women and students of color ended up paying more for the same loan, or being denied access to credit. (Read more here.) So keep an eye on all this.

CBA was also sort of being cute in the document about wanting a return of government guarantees for private student loans. Like, they included a pretty detailed discussion of them, then sort of said “well we aren’t RECOMMENDING you bring them back, uwu.” Ugh.

The crypto market structure bill came out of committee in the Senate on a party-line vote, but the vibes still aren’t great.

Recall: the crypto people have been pushing a bill called the CLARITY Act (people call it the “crypto market structure” bill) that would more or less finish the work of creating a formal (if still super light-touch) regulatory regime for crypto.

But a big fight has emerged (detail here) over whether stablecoin issuers can pay consumers things called “rewards.” The problem is that those rewards basically look like interest payments, which supports the idea that stablecoins are actually unregulated and very dangerous deposit accounts. The Senate Ag committee voted this past week on a version of the CLARITY Act that more or less splits the baby on “rewards”:

The proposal includes language that would appear to prohibit crypto exchanges from offering rewards tied to stablecoin holdings. But the bill also highlights some activities that would be exempt from that restriction, including certain rewards associated with membership in a loyalty or incentive program.

This bill still has a long way to go, and in the background folks are mad about all of it. E.g., the Journal reports on bank CEOs in Davos being mad at crypto people (emphasis added):

“You are full of s—,” said Dimon, a longtime crypto skeptic who previously called bitcoin a fraud, his index finger pointed squarely at [Coinbase CEO Brian] Armstrong’s face.

. . .

“If you want to be a bank, just be a bank,” Bank of America chief executive Brian Moynihan told Armstrong during a cordial but somewhat stilted 30-minute meeting last week at the main convention center in Davos. “If you want to be a money-market fund, just be a money-market fund.”

I do have to say it’s fun to watch two extremely entitled, whiny, and well-monied interest groups be at such direct odds. I just hope consumers come out okay.

Elsewhere: Politico profiles how Bessent is breaking from former Treasury secretaries in actively pushing independent bank regulators to adopt a light-touch approach, and is otherwise calling for “a fundamental reset of financial regulation.”

Credit card stuff continues.

When we last spoke, I said that Senator Marshall’s Credit Card Competition Act (CCCA) appeared to be gaining momentum against the backdrop of Trump’s call for a 10 percent rate cap. Detail on that bill here. Well last week Marshall tried to add the CCCA as an amendment to the crypto bill discussed above, but he ultimately nixed that idea. Now we wait.

Discourse on the proposed 10 percent rate cap continues. E.g., e.g., e.g., e.g.

Understanding how the world operates in 2026, Visa announced it would “work with its bank partners to add the option of using rewards to save in so-called ‘Trump accounts.’” Trump Accounts are a kind of tax-advantaged savings account for kids that were created in the Big Bill. And yes, the name “Trump Account” is actually in the statute.

And finally, some potpourri:

Warsh gets the Fed Chair nod. Some takes:

Funny: Cliff Asness at AQR.

Negative, if from 2017: How to be wrong about almost everything and maybe be Fed chair anyway: the Kevin Warsh story.

Very negative, from Krugman: A Bad Heir Day at the Fed

Warsh is a political animal. He calls for tight money and opposes any attempt to boost the economy when Democrats hold the White House. Like all Trumpers, he has been all for lower interest rates since November 2024.

The Center for Responsible Lending has a great new report on OppFi, an online lender that “charges exorbitant rates on personal installment loans, with APRs of up to 195%” through the clever use of “Rent A Bank Schemes.” (h/t Whitney Barkley-Denney, Andrew Kushner, and Candice Wang)

The CEO of PNC was on Odd Lots. He mostly said what you’d expect, except he forgot his message discipline a bit when it came to the company line that the evil Bidens stood in the way of purportedly good bank mergers. E.g., he said (this is from the YouTube transcript and I cleaned it up a bit):

[T]he weird window in regulatory change isn’t the Trump administration. It was the Biden administration. . . [N]ow after Biden, [merger] deals get done all the time.

But he also said (cleaned up, emphasis added):

[O]ne of those sound bites that comes out [is that] regulators [say] “good deals are okay, bad deals aren’t,” but they won’t tell you what a bad deal is. But a good deal is typically when you have one bank, someone good [at that] bank, somebody in charge. You have technology that can actually absorb the other bank. And you can protect consumers and so on and so forth. Those could have gotten done in the last administration.

So like, you agree that the Bidens only stood in the way of bad mergers? And were unique in doing so?

I hesitated to put this in here, but I must:

An absolute must-read on the LPE blog: The Means Testing Industrial Complex by Luke Farrell. Just one bit from that (emphasis added):

Since Georgia implemented work requirements in 2020, they have spent twice as much on Deloitte consultants and administrative costs as on healthcare for people. As the other 55 states and territories are now forced to join Georgia and implement new work requirements, millions will lose their healthcare and Deloitte will cash in.

Trump says he wants to drive housing prices up, not down.

“Biden created the largest surge in US manufacturing investment in decades. Trump cancelled it.”

New 30 under 30 indictment drops:

A Turkish tech executive who launched a New York “fintech marketing” firm to create rewards programs for dozens of brands has been indicted for bilking venture capitalists of $7 million in seed money and using the proceeds to secure an O-1A “extraordinary ability” visa last fall.

Related, in Semafor: An entrepreneur’s 13 hours in Davos jail: ‘The food was phenomenal.’

Moderna “curbing” investment in vaccine trials due to political backlash.

BBerg: China’s Retreat From Africa Lending Turns It Into Debt Collector

Science: U.S. government has lost more than 10,000 STEM Ph.D.s since Trump took office

Domestic migration to Florida falls 90 percent from 2022 to 2025.

Limited edition $280 Amtrak Trak Suit (available through today!)

Steak ‘n Shake Adds $5M in BTC Exposure, Amid Burger-to-Bitcoin Transformation (something something “buy the dip,” h/t Mike Pierce).

“Nothing in governmental logos will ever beat mid-century NYC.”

Have a great week!

| A guest post by

|

Brilliant piece. The Kardashian Kard story perfectly captures how predatory fintech can weaponize celebrity appeal against vulnerable consumers, and it feels especially relevant given the CFPB changes covered later. I ran into a similar fee structrue years back with a prepaid card at a small business, and the compounding costs were insane once you realized what was happening.